Industrial machinery company Generac Holdings Inc. (GNRC) in Waukesha, Wisc., designs, manufactures and sells power generation equipment, energy storage systems, and other power products. The company’s offerings include engines, alternators, batteries, and residential automatic standby generators.

GNRC has raised the prices of its standby generators over the past 15 to 18 months. The price rises have partly covered its increased logistics, labor, and raw materials costs. However, demand for the generators does not seem to have been dampened as the company saw higher-than-expected shipments of the home standby generators for the quarter ended March 31. GNRC is planning another price increase, effective June 1.

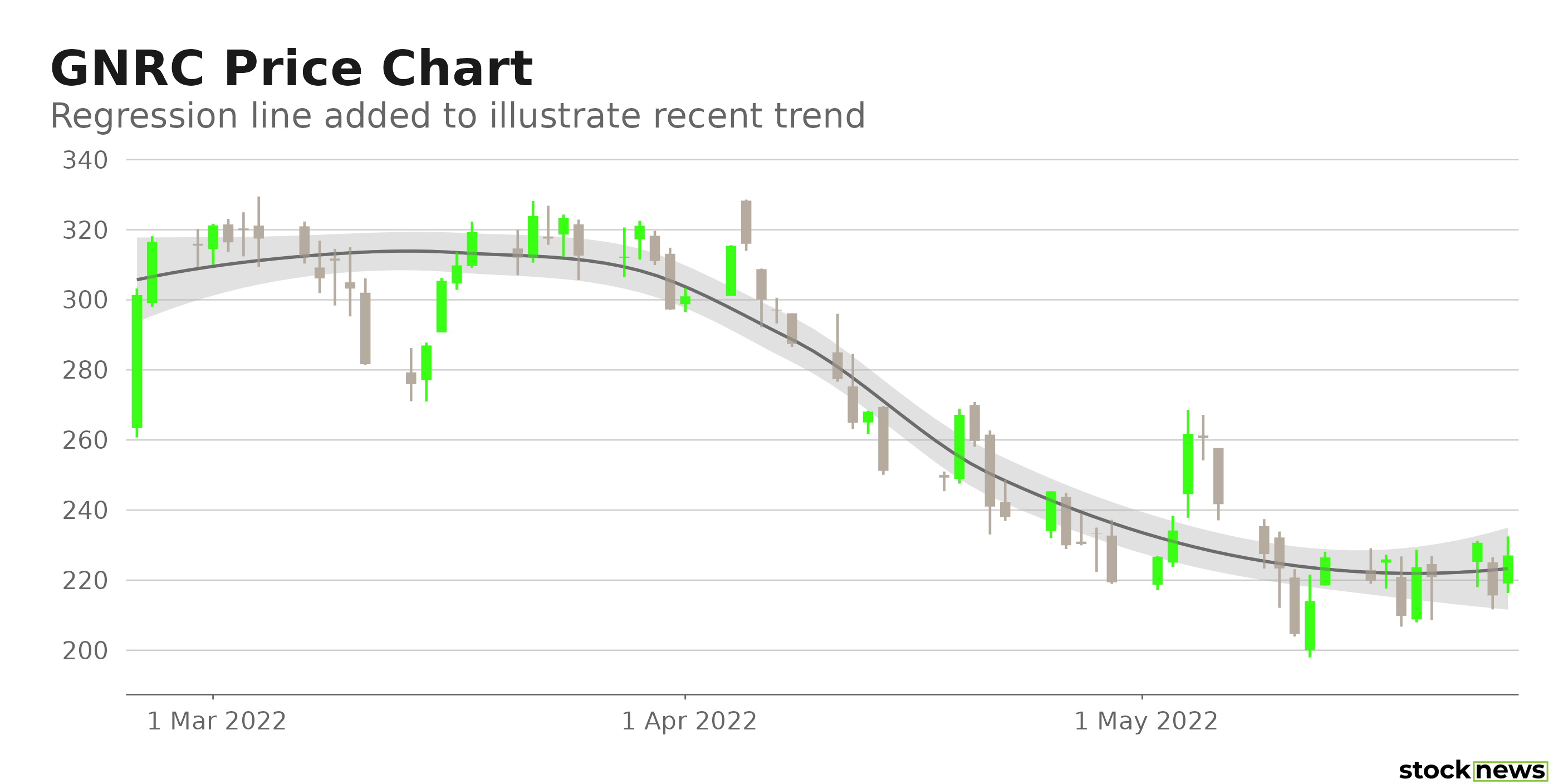

However, GNRC’s stock has declined 30.6% in price over the past year and 38.7% year-to-date to close yesterday’s trading session at $215.63. It has declined 9.4% over the past month.

Here are the factors that could affect GNRC’s performance in the near term:

Mixed Financials

For its fiscal first quarter, ended March 31, GNRC’s net sales increased 40.7% year-over-year to $1.14 billion. Its gross profit rose 12.1% from the prior-year quarter to $360.75 million. However, its adjusted net income decreased 9.9% from the same period the prior year to $138.76 million, while its adjusted net income attributable to GNRC per common share declined 12.2% from the prior-year period to $2.09.

Favorable Analyst Expectations

The $2.62 consensus EPS estimate for the quarter ending June 30, 2022, indicates a 9.6% year-over-year increase. And the $1.27 billion consensus revenue estimate for the same quarter reflects a 37.9% improvement from the prior-year quarter.

The Street’s $3.17 EPS estimate for the quarter ending Sept. 30, 2022, indicates a 34.9% year-over-year rise. And the Street’s $1.33 billion revenue estimate for the same quarter reflects a 40.9% increase from the prior-year period.

Stretched Valuations

In terms of its forward EV/Sales, GNRC is currently trading at 2.94x, which is 87.3% higher than the 1.57x industry average. The stock’s 2.85 forward Price/Sales multiple is 129% higher than the 1.24 industry average. And in terms of its forward Price/Book, it is trading at 5.11x, which is 101.8% higher than the 2.54x industry average.

Mixed Profit Margins

GNRC’s trailing 12-month gross profit margin and net income margin of 34.41% and 12.68%, respectively, are 16.6% and 87.4% higher than their respective industry averages of 29.51% and 6.76%. Its trailing 12-month ROE, ROTC, and ROA of 25.37%, 14.30%, and 10.00%, respectively, are 75.2%, 97.7%, and 85.2% higher than the 14.48%, 7.23% and 5.40% industry averages. However, its trailing 12-month levered FCF margin of 3.14% is 11.2% lower than the 3.54% industry average.

POWR Ratings Reflect Uncertain Prospects

GNRC has an overall C rating, which equates to Neutral in our proprietary POWR Ratings system. The POWR Ratings are calculated by considering 118 distinct factors, with each factor weighted to an optimal degree.

GNRC has a Growth grade of C, which is in sync with its mixed growth in the last reported quarter. The stock has a D grade for Stability, which is consistent with its five-year monthly beta of 1.15.

GNRC has a C grade for Quality, which is justified by its mixed profitability margins.

In the 80-stock Industrial – Machinery industry, it is ranked #68. The industry is rated B.

Click here to see the additional POWR Ratings for GNRC (Value, Momentum, and Sentiment).

View all the top stocks in the Industrial – Machinery industry here.

Click here to check out our Industrial Sector Report for 2022

Bottom Line

GNRC experienced robust demand and reported solid revenue growth in its most recent quarter. However, the company’s top-line growth did not translate to bottom-line improvement. Furthermore, GNRC looks overvalued at its current price, and its high beta indicates volatility in the stock. Thus, I think it might be wise to wait for a better entry point in the stock.

How Does Generac Holdings Inc. (GNRC) Stack Up Against its Peers?

While GNRC has an overall POWR Rating of C, one might consider looking at its industry peers, THK Co., Ltd. (THKLY) and Mitsubishi Heavy Industries, Ltd. (MHVYF), which have an overall A (Strong Buy) rating, and Amada Co., Ltd. (AMDLY) and Tennant Company (TNC), which have an overall B (Buy) rating.

GNRC shares were trading at $227.44 per share on Wednesday morning, up $11.81 (+5.48%). Year-to-date, GNRC has declined -35.37%, versus a -16.53% rise in the benchmark S&P 500 index during the same period.

About the Author: Anushka Dutta

Anushka is an analyst whose interest in understanding the impact of broader economic changes on financial markets motivated her to pursue a career in investment research.

The post Down More Than 30% in the Past Year, is Now a Good Time to Buy Generac Holdings? appeared first on StockNews.com