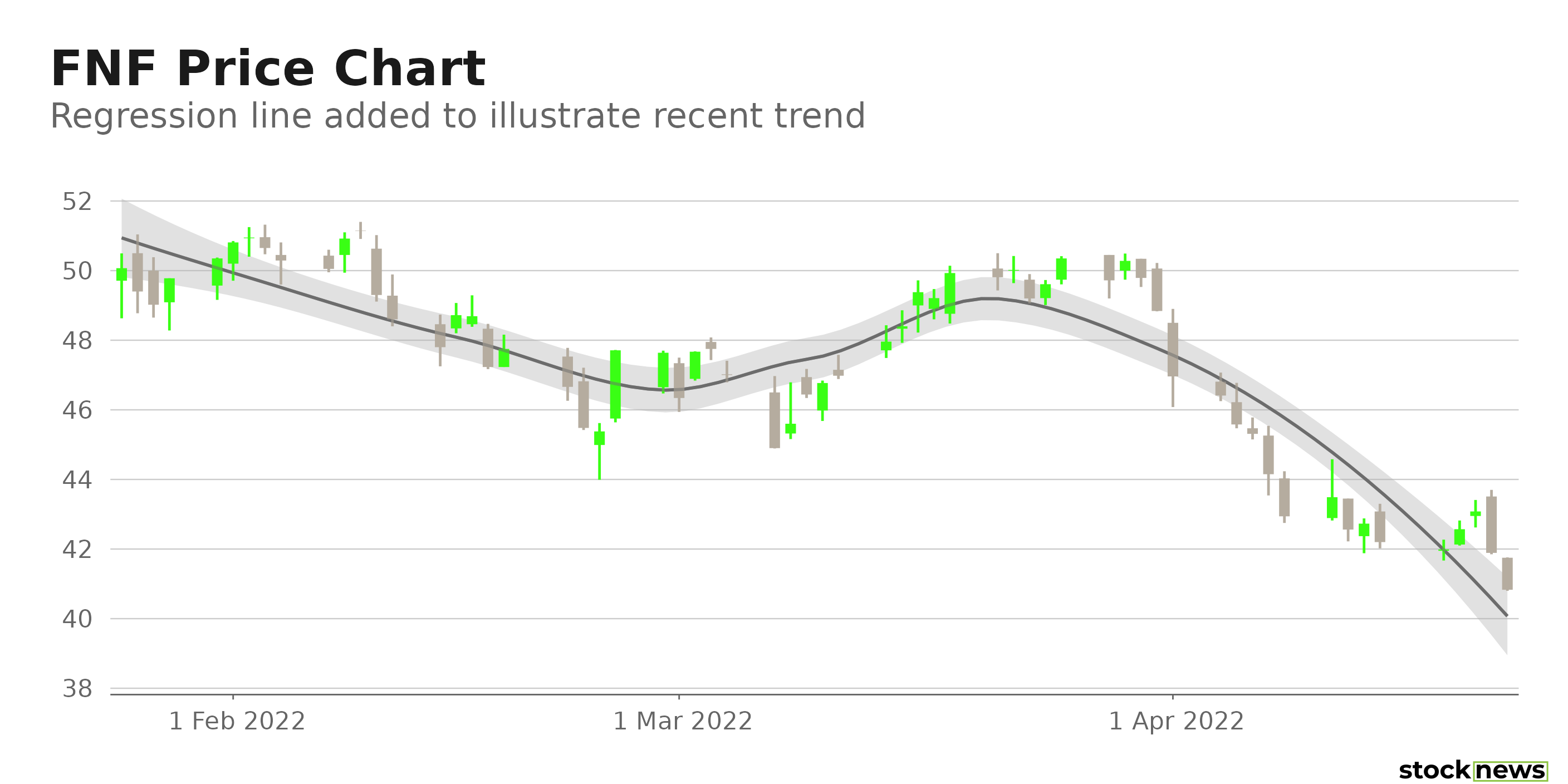

Jacksonville, Fla.-based title insurance and transaction services provider to the real estate and mortgage industries, Fidelity National Financial, Inc. (FNF), offers various insurance products, including trust activities, trustee sales guarantees, reconveyances, and home warranty insurance. The settlement services provider’s stock has dipped 17.1% in price over the past month and 20.6% year-to-date, due mainly to bearish investor sentiment surrounding the real estate market amid growing recession worries.

While FNF’s direct title premiums rose 21% year-over-year to $1 billion, the company’s refinance orders have declined 39% daily from the fourth quarter of 2020. Furthermore, earlier this month, the Federal Reserve Bank of Dallas issued a warning about the property market showing signs of “a brewing bubble.”

Although continuing strong asset growth, momentum in commercial revenue, and record-level performance in the Title business have helped FNF deliver attractive returns to its shareholders, a decline in refinance volumes and its elevated operational expenses could hinder its market-share growth. Also, its weak profitability could cause its shares to retreat further.

Here is what could influence FNF’s performance in the coming months:

Unstable Property Market

While the housing market continues to be red hot amid surging prices and rising mortgage rates, worries surrounding a potential crash could lead to a negative sentiment among investors. According to Redfin, the rate of sellers lowering their asking prices has been growing fast since last year. The cooling of housing prices could, in turn, negatively affect mortgage insurance companies.

In addition, growing inflationary pressure and potential Fed action could significantly increase mortgage interest rates, thereby lowering the number of borrowers expected to refinance. This could hurt FNF’s refinance volumes.

Mixed Growth Potential

Analysts expect FNF’s revenues to increase 20.3% in the next quarter (ending June 2022) and 2.7% next year. But its revenue is estimated to decline 18% year-over-year to $12.83 billion in its fiscal 2022. The company’s EPS is expected to decline 22.3% year-over-year to $1.6 next quarter and 22.8% year-over-year to $6.1 in the current year. However, its EPS is expected to increase 4.3% in fiscal 2023.

Mixed Financials

FNF’s total sales from the F&G business increased 50% year-over-year to $2.2 billion in the fourth quarter, ended Dec. 31, 2021. Its retail sales came in at $1.4 billion, representing 5% growth from the prior-year period. However, the title insurance provider’s net earnings under F&G stood at $121 million for the quarter, down 11.7% year-over-year. Also, FNF’s total opened orders declined 22.1% sequentially.

Poor Profitability

Its 10.5% trailing-12-month levered free cash flow margin is 53.9% lower than the 22.7% industry average. FNF’s net income margin and EBIT margin of 15.5% and 20.5%, respectively, are 48.7% and 24.1% lower than their industry averages. In addition, its 59.4% gross profit margin is 11.4% lower than the 67.1% industry average.

POWR Ratings Reflect Uncertainty

FNF has an overall rating of C, which translates to Neutral in our POWR Ratings system. The POWR Ratings are calculated by considering 118 distinct factors, with each factor weighted to an optimal degree.

Our proprietary rating system also evaluates each stock based on eight distinct categories. FNF has a C grade for Quality. The stock’s weak profitability is in sync with this grade.

Furthermore, the company has a Momentum grade of C, which is consistent with its price returns over the past month.

And in terms of Stability Grade, FNF has a C. This justifies the stock’s relatively high beta of 1.36.

In addition to the grades I’ve highlighted, one can check out additional FNF ratings for Value, Sentiment, and Growth here. FNF is ranked #4 of 6 stocks in the C-rated Insurance - Title industry.

Bottom Line

The record top-line performance of FNF’s title insurance business and strong asset growth across its F&G business segment have boosted the leading title insurance company’s title-premium growth and revenues. However, an expected contraction in refinance volumes and growing concerns surrounding the development of a real estate market bubble have added uncertainties to its prospects. Therefore, we think investors should wait for the situation to stabilize before investing in the stock.

How Does Fidelity National Financial (FNF) Stack Up Against its Peers?

While FNF has an overall C rating in our proprietary rating system, one might want to consider taking a look at its industry peer, Investors Title Company (ITIC), having an A (Strong Buy) rating.

FNF shares were unchanged in premarket trading Monday. Year-to-date, FNF has declined -21.03%, versus a -10.02% rise in the benchmark S&P 500 index during the same period.

About the Author: Imon Ghosh

Imon is an investment analyst and journalist with an enthusiasm for financial research and writing. She began her career at Kantar IMRB, a leading market research and consumer consulting organization.

The post Should You Buy the Dip in Fidelity National Financial Stock? appeared first on StockNews.com