Midwest regional bank QCR Holdings (NASDAQGM:QCRH) met Wall Streets revenue expectations in Q4 CY2025, with sales up 2.8% year on year to $107 million. Its non-GAAP profit of $2.21 per share was 11.3% above analysts’ consensus estimates.

Is now the time to buy QCR Holdings? Find out by accessing our full research report, it’s free.

QCR Holdings (QCRH) Q4 CY2025 Highlights:

- Net Interest Income: $68.35 million vs analyst estimates of $68.31 million (11.7% year-on-year growth, in line)

- Net Interest Margin: 3.1% vs analyst estimates of 3.6% (51 basis point miss)

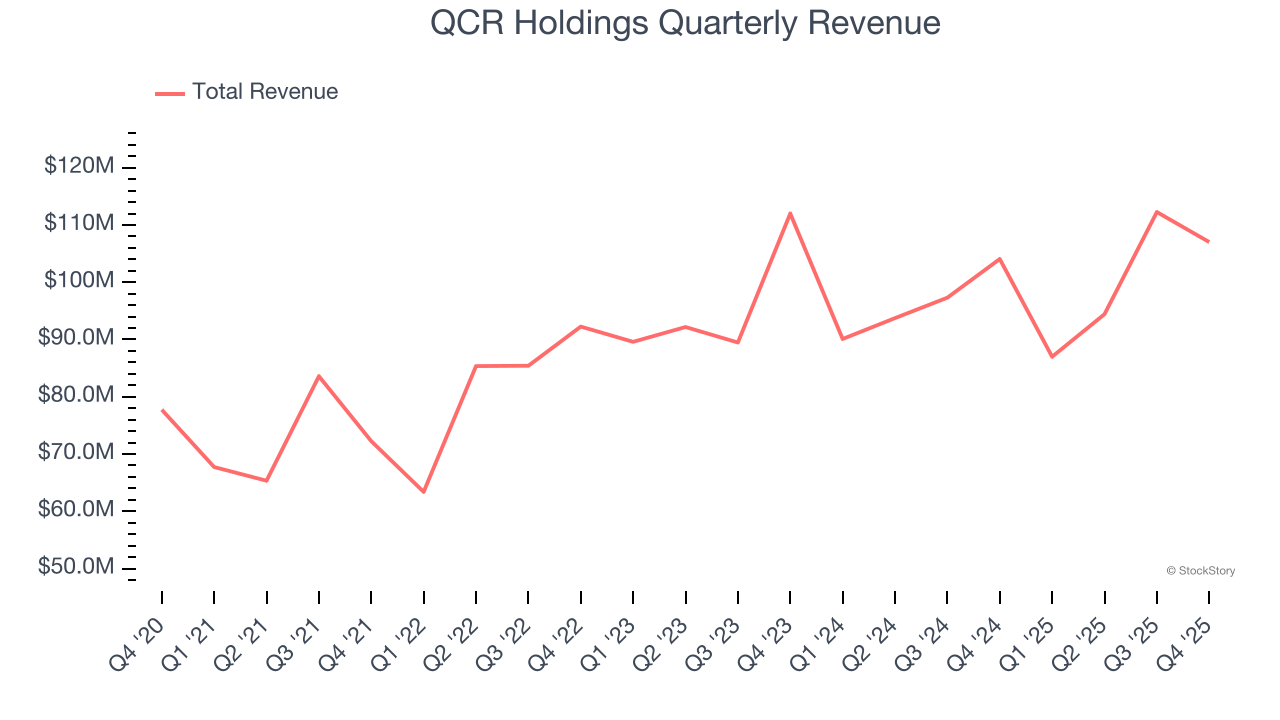

- Revenue: $107 million vs analyst estimates of $106.9 million (2.8% year-on-year growth, in line)

- Efficiency Ratio: 58.7% vs analyst estimates of 53.3% (542.8 basis point miss)

- Adjusted EPS: $2.21 vs analyst estimates of $1.99 (11.3% beat)

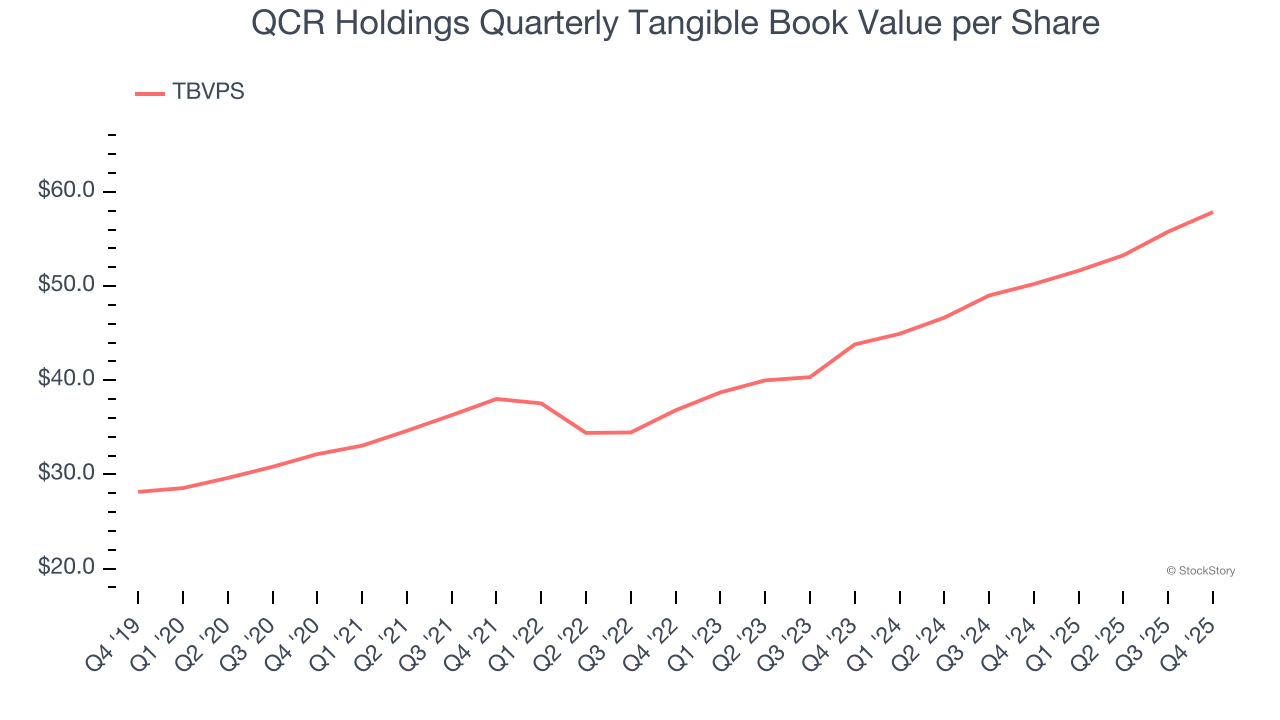

- Tangible Book Value per Share: $57.86 vs analyst estimates of $57.68 (15.2% year-on-year growth, in line)

- Market Capitalization: $1.47 billion

“We delivered our strongest quarter and record full year results as we continue to see improved performance in our traditional banking, wealth management, and LIHTC lending businesses. At the same time, we continued to invest in our digital transformation project, creating the bank of the future for our clients and our employees,” said Todd Gipple, President and Chief Executive Officer.

Company Overview

With roots dating back to 1993 and a name reflecting its original Quad Cities market, QCR Holdings (NASDAQGM:QCRH) operates four community banks across Iowa and Missouri, providing commercial, consumer banking, and trust services to businesses and individuals.

Sales Growth

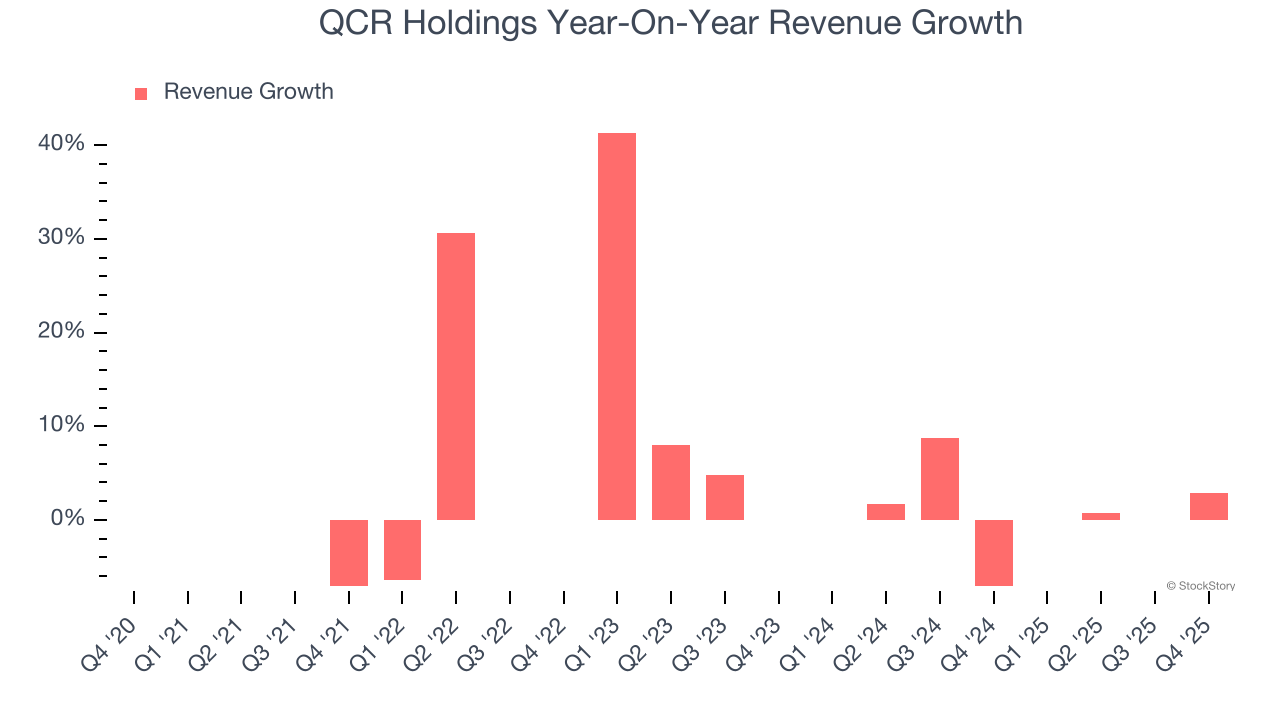

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Over the last five years, QCR Holdings grew its revenue at a tepid 7% compounded annual growth rate. This was below our standard for the banking sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. QCR Holdings’s recent performance shows its demand has slowed as its annualized revenue growth of 2.2% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, QCR Holdings grew its revenue by 2.8% year on year, and its $107 million of revenue was in line with Wall Street’s estimates.

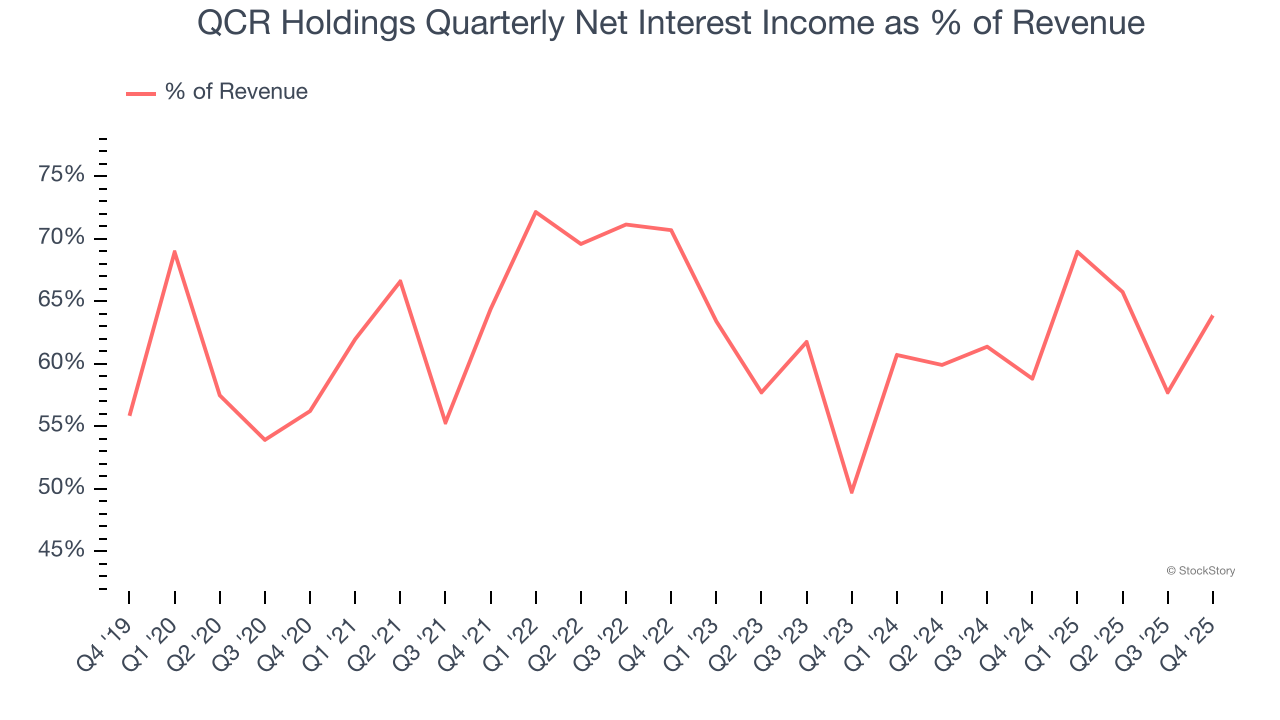

Net interest income made up 63.1% of the company’s total revenue during the last five years, meaning lending operations are QCR Holdings’s largest source of revenue.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

QCR Holdings’s TBVPS grew at an incredible 12.5% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 14.9% annually over the last two years from $43.81 to $57.86 per share.

Over the next 12 months, Consensus estimates call for QCR Holdings’s TBVPS to grow by 12.8% to $65.26, decent growth rate.

Key Takeaways from QCR Holdings’s Q4 Results

It was good to see QCR Holdings beat analysts’ EPS expectations this quarter. Overall, this print had some key positives. The stock remained flat at $88.06 immediately after reporting.

Big picture, is QCR Holdings a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).