Over the past six months, Erie Indemnity’s shares (currently trading at $359.82) have posted a disappointing 7.8% loss, well below the S&P 500’s 6.4% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is now the time to buy ERIE? Find out in our full research report, it’s free.

Why Is ERIE a Good Business?

Operating under a unique business model dating back to 1925, Erie Indemnity (NASDAQ: ERIE) serves as the attorney-in-fact for Erie Insurance Exchange, managing policy issuance, claims handling, and investment services for this reciprocal insurer.

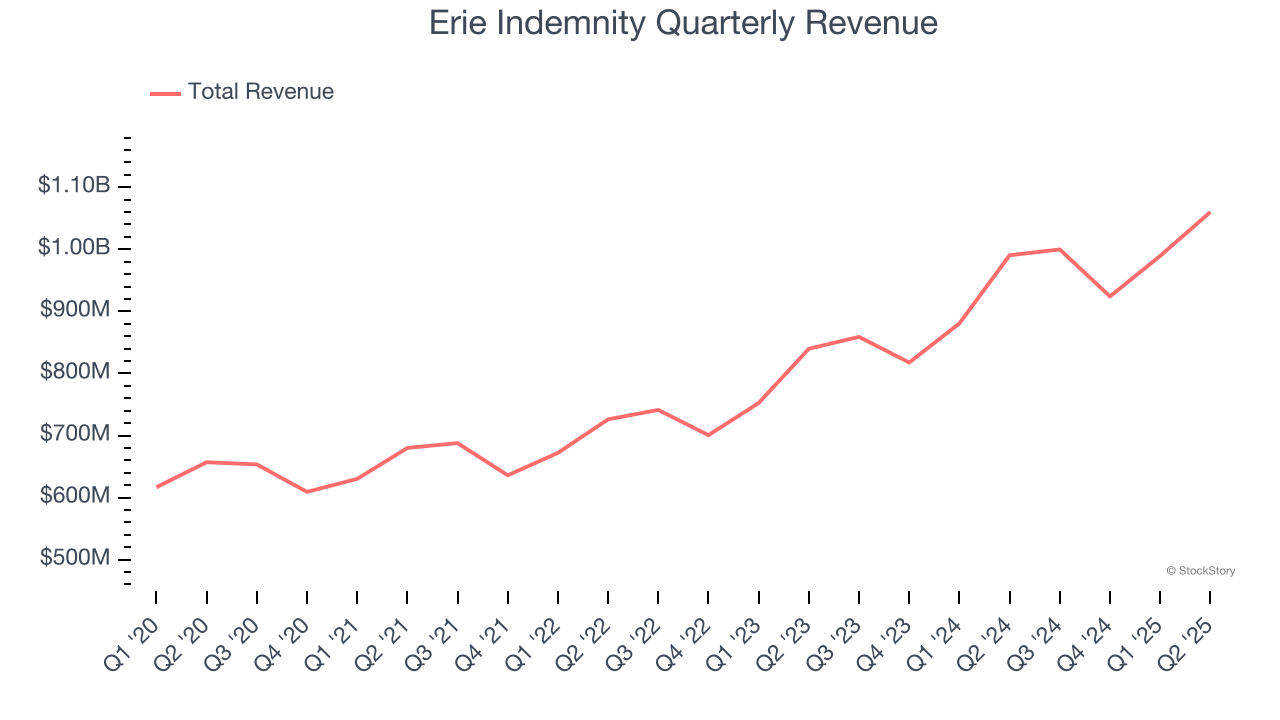

1. Long-Term Revenue Growth Shows Strong Momentum

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services.

Thankfully, Erie Indemnity’s 10% annualized revenue growth over the last five years was solid. Its growth beat the average insurance company and shows its offerings resonate with customers.

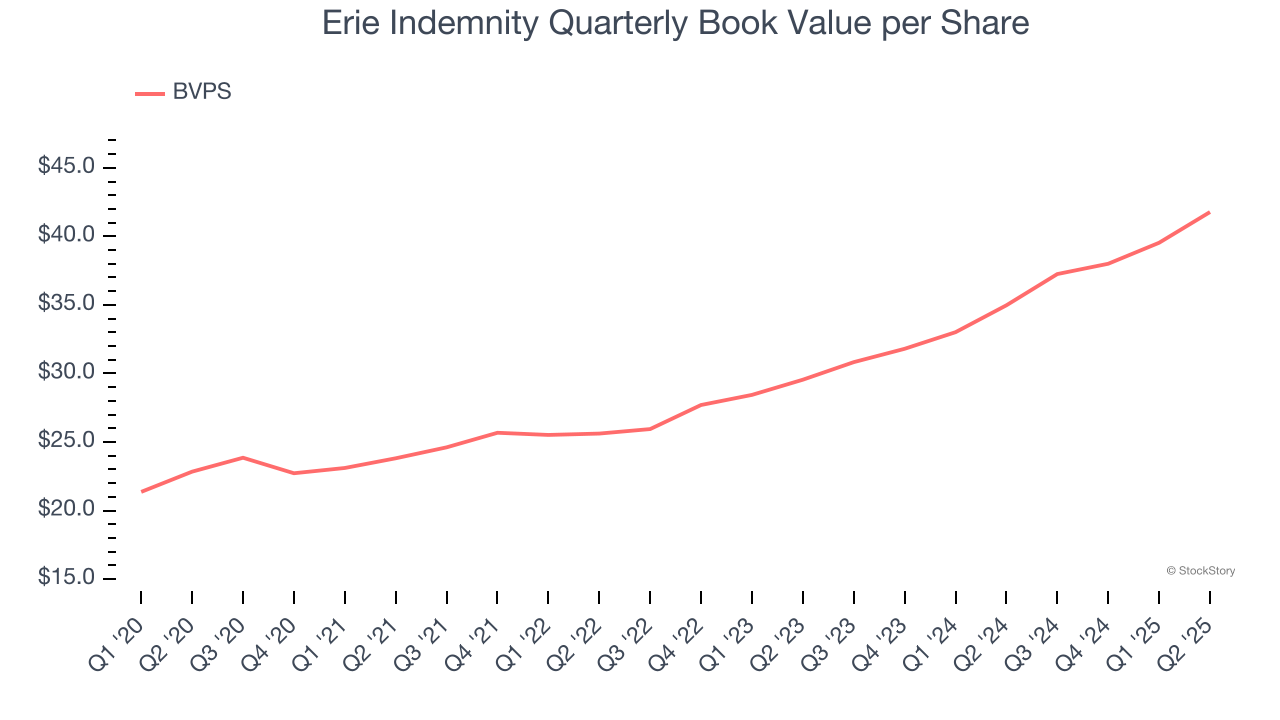

2. Growing BVPS Reflects Strong Asset Base

In the insurance industry, book value per share (BVPS) provides a clear picture of shareholder value, as it represents the total equity backing a company’s insurance operations and growth initiatives.

Erie Indemnity’s BVPS increased by 12.8% annually over the last five years, and growth has recently accelerated as BVPS grew at an impressive 18.9% annual clip over the past two years (from $29.55 to $41.78 per share).

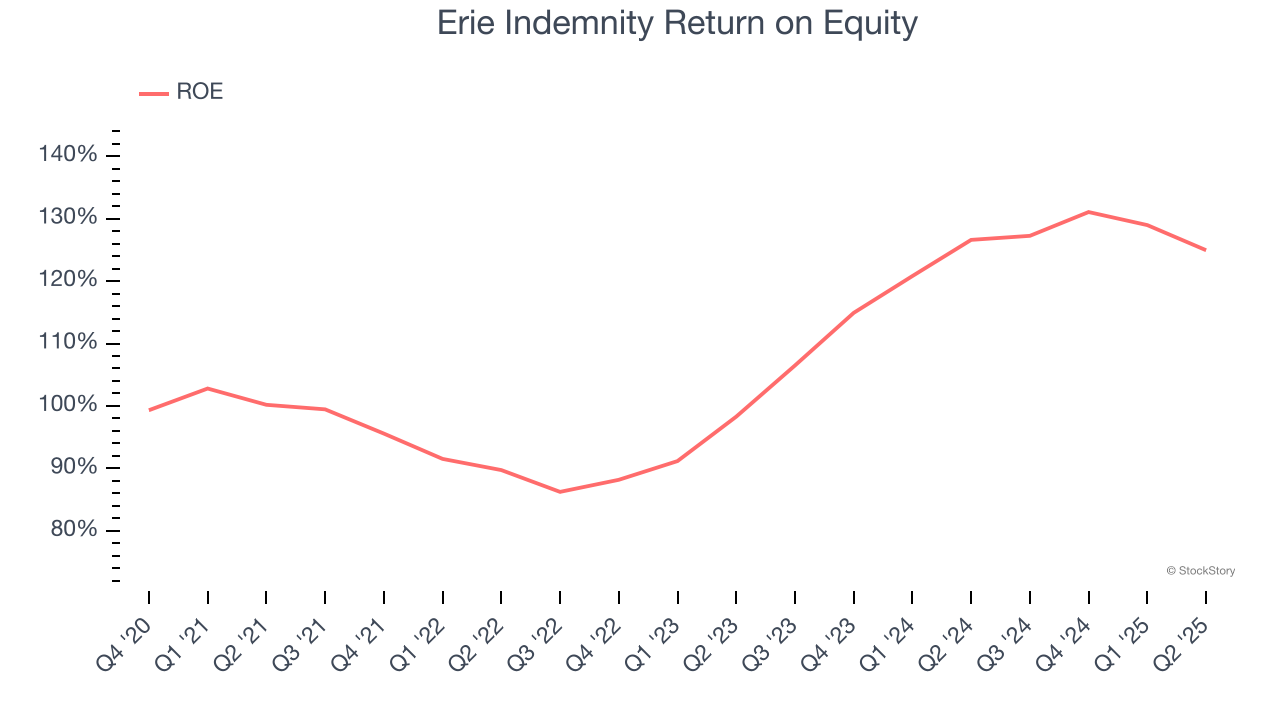

3. Stellar ROE Showcases Lucrative Growth Opportunities

Return on Equity, or ROE, ties everything together and is a vital metric. It tells us how much profit the insurer generates for each dollar of shareholder equity entrusted to management. Over a long period, insurers with higher ROEs tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Erie Indemnity has averaged an ROE of 27%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows Erie Indemnity has a strong competitive moat.

Final Judgment

These are just a few reasons why we think Erie Indemnity is one of the best insurance companies out there. With the recent decline, the stock trades at $359.82 per share (or a trailing 12-month price-to-sales ratio of 4.7×). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Erie Indemnity

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.