Zimmer Biomet has been treading water for the past six months, recording a small loss of 1.6% while holding steady at $101.84. However, the stock is beating the S&P 500’s 9.8% decline during that period.

Is now the time to buy Zimmer Biomet, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even with the strong relative performance, we don't have much confidence in Zimmer Biomet. Here are three reasons why we avoid ZBH and a stock we'd rather own.

Why Is Zimmer Biomet Not Exciting?

With a history dating back to 1927 and a presence in over 100 countries worldwide, Zimmer Biomet (NYSE: ZBH) designs and manufactures orthopedic products including knee and hip replacements, surgical tools, and robotic technologies for joint reconstruction and spine surgeries.

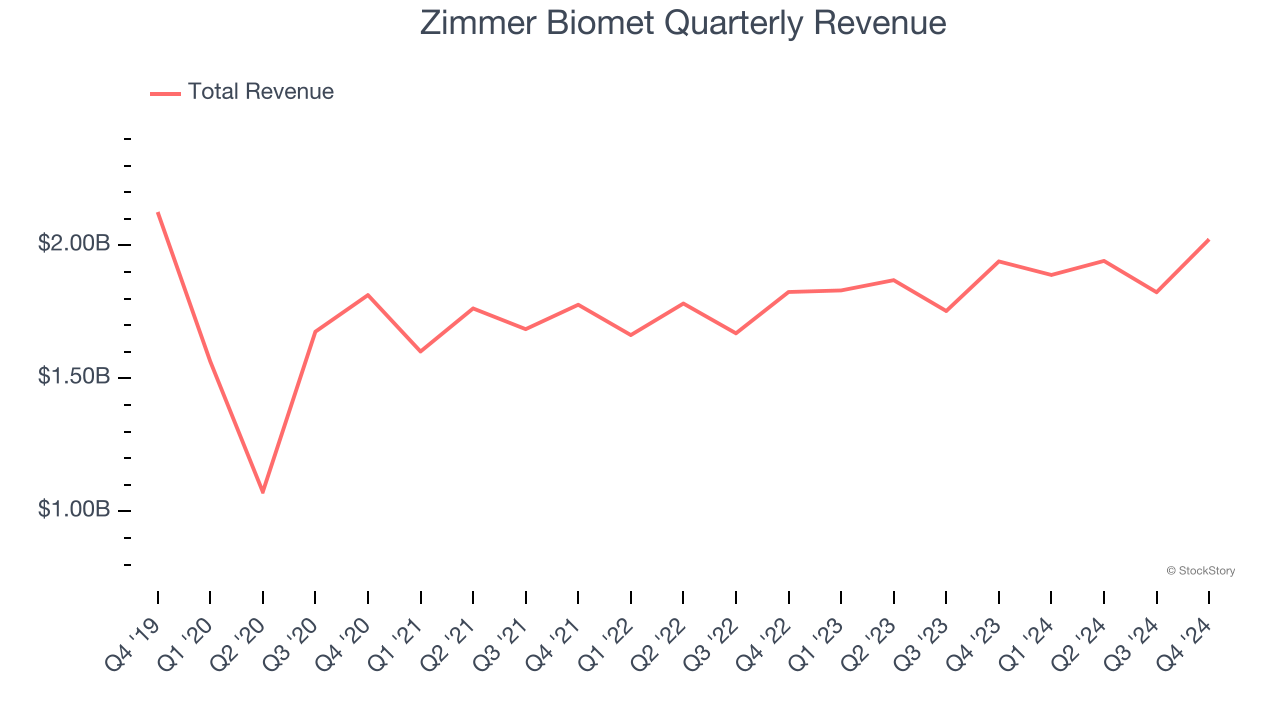

1. Long-Term Revenue Growth Flatter Than a Pancake

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Zimmer Biomet struggled to consistently increase demand as its $7.68 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of lacking business quality.

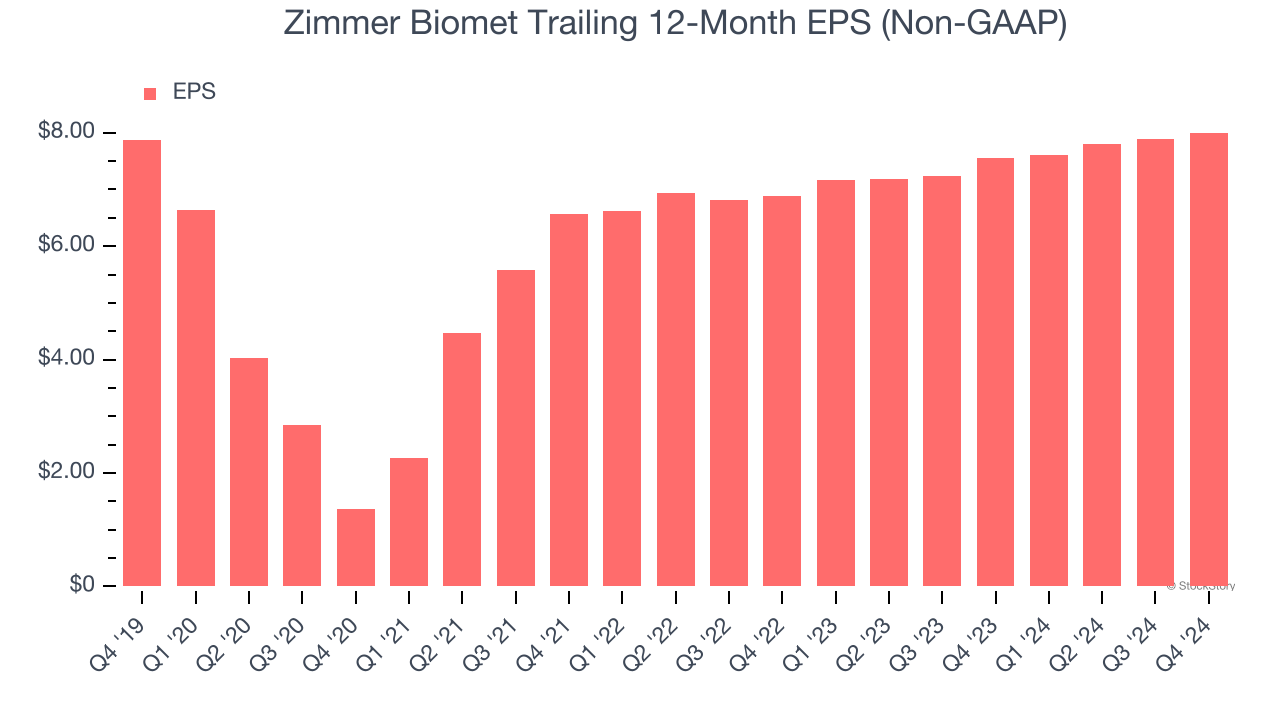

2. EPS Growth Has Stalled

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Zimmer Biomet’s EPS was flat over the last five years, just like its revenue. This performance was underwhelming across the board.

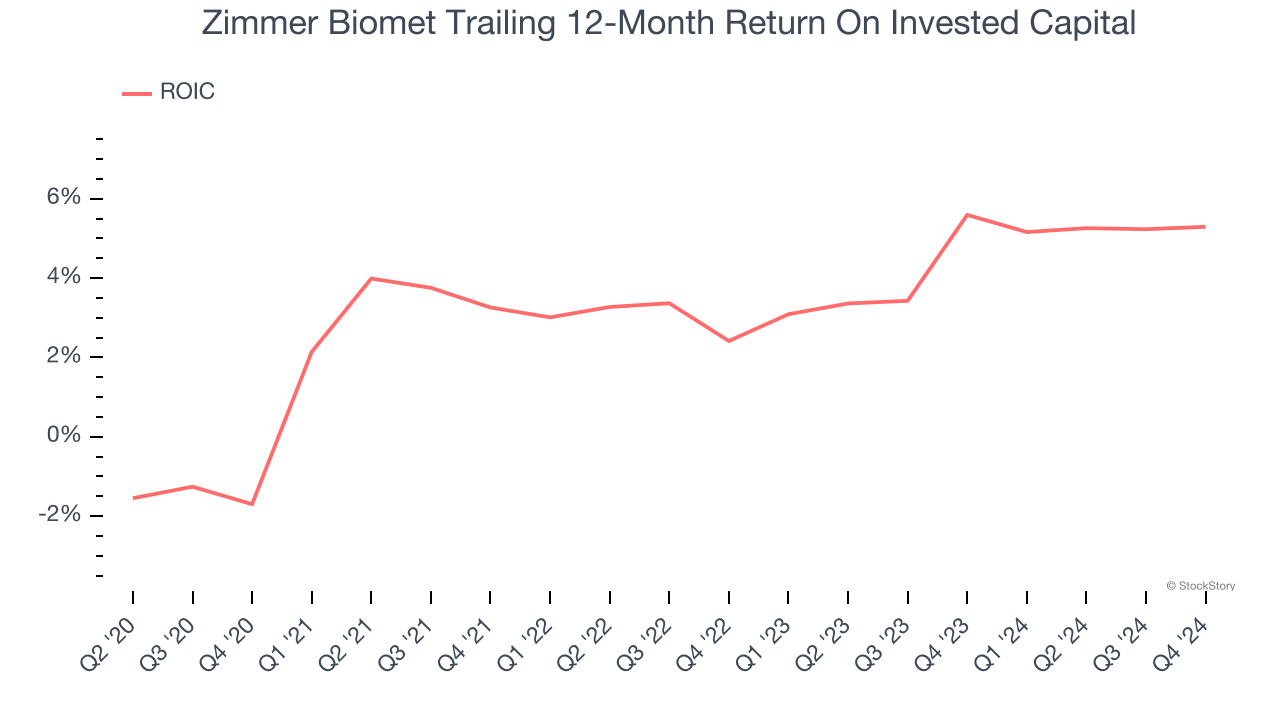

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Zimmer Biomet historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

Final Judgment

Zimmer Biomet isn’t a terrible business, but it doesn’t pass our quality test. Following its recent outperformance in a weaker market environment, the stock trades at 11.9× forward price-to-earnings (or $101.84 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Zimmer Biomet

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.