Over the past six months, Zoetis’s shares (currently trading at $166) have posted a disappointing 9.6% loss, well below the S&P 500’s 7.6% gain. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is now an opportune time to buy ZTS? Find out in our full research report, it’s free.

Why Does ZTS Stock Spark Debate?

Originally a subsidiary of Pfizer, Zoetis (NYSE: ZTS) is an animal health company that develops and distributes medicines, vaccines, and diagnostic products for livestock and pets.

Two Things to Like:

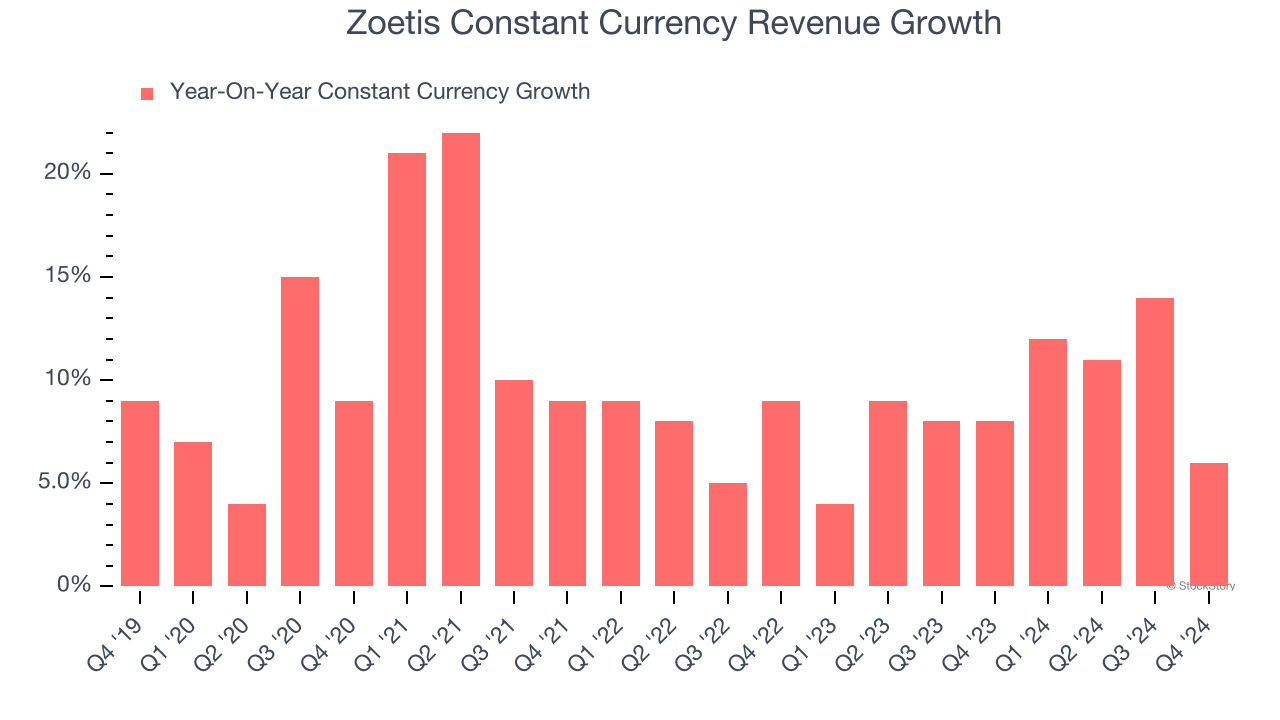

1. Constant Currency Revenue Drives Growth

In addition to reported revenue, constant currency revenue is a useful data point for analyzing Branded Pharmaceuticals companies. This metric excludes currency movements, which are outside of Zoetis’s control and are not indicative of underlying demand.

Over the last two years, Zoetis’s constant currency revenue averaged 9% year-on-year growth. This performance was solid and shows it can expand steadily on a global scale regardless of the macroeconomic environment.

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Zoetis’s five-year average ROIC was 28.7%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to be Careful:

Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Zoetis’s revenue to stall, a deceleration versus its 7% annualized growth for the past two years. This projection is underwhelming and implies its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Final Judgment

Zoetis’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 26.9× forward price-to-earnings (or $166 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Zoetis

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.