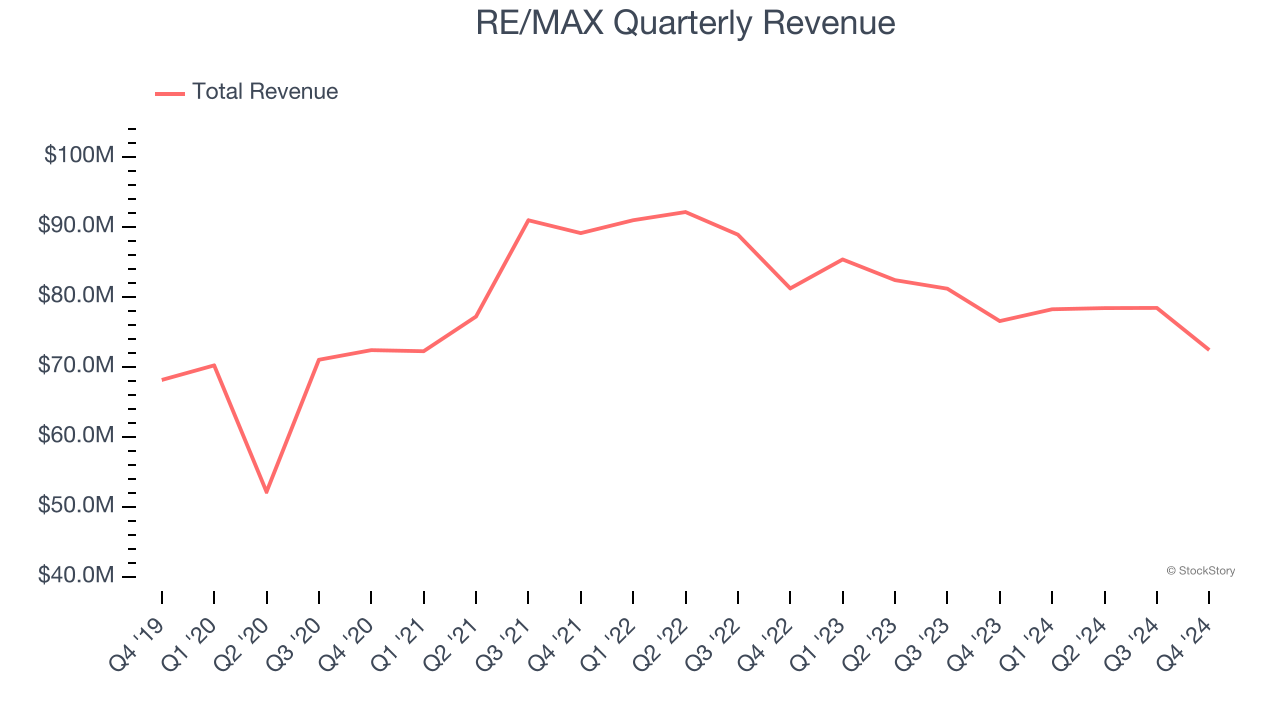

Real estate franchise company RE/MAX (NYSE: RMAX) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 5.4% year on year to $72.47 million. Next quarter’s revenue guidance of $73.5 million underwhelmed, coming in 5.8% below analysts’ estimates. Its non-GAAP profit of $0.30 per share was 4.8% above analysts’ consensus estimates.

Is now the time to buy RE/MAX? Find out by accessing our full research report, it’s free.

RE/MAX (RMAX) Q4 CY2024 Highlights:

- Revenue: $72.47 million vs analyst estimates of $74.5 million (5.4% year-on-year decline, 2.7% miss)

- Adjusted EPS: $0.30 vs analyst estimates of $0.29 (4.8% beat)

- Adjusted EBITDA: $23.34 million vs analyst estimates of $22.66 million (32.2% margin, 3% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $300 million at the midpoint, missing analyst estimates by 3.5% and implying -2.5% growth (vs -5.5% in FY2024)

- EBITDA guidance for the upcoming financial year 2025 is $95 million at the midpoint, below analyst estimates of $97.26 million

- Operating Margin: 5.9%, up from -12.7% in the same quarter last year

- Free Cash Flow Margin: 22.1%, up from 8.4% in the same quarter last year

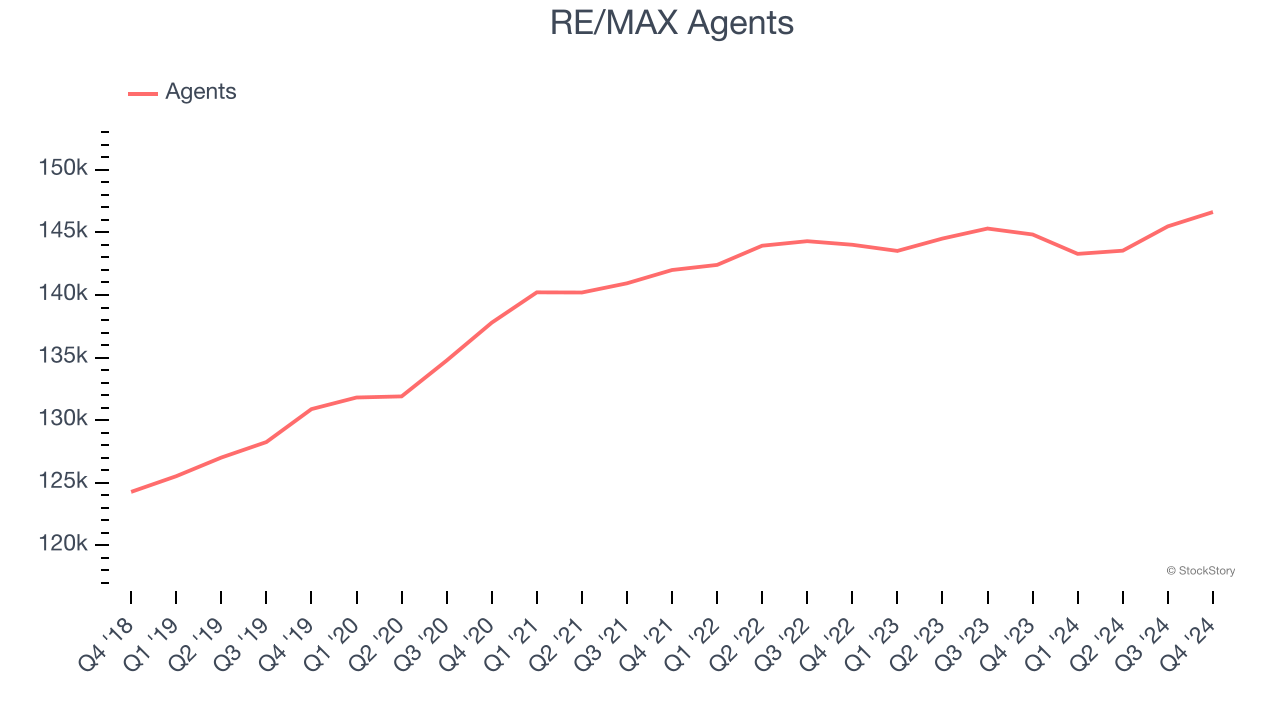

- Agents: 146,627, up 1,792 year on year

- Market Capitalization: $197.6 million

Company Overview

Short for Real Estate Maximums, RE/MAX (NYSE: RMAX) operates a real estate franchise network spanning over 100 countries and territories.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

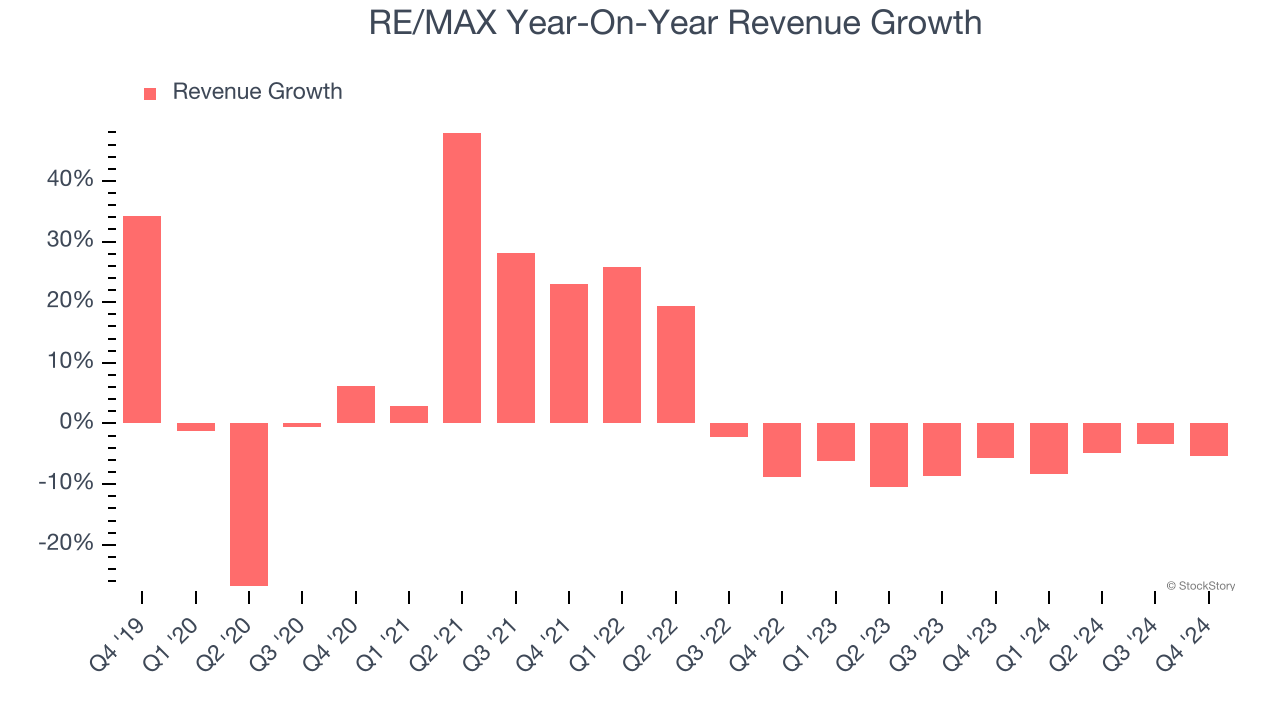

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Unfortunately, RE/MAX’s 1.7% annualized revenue growth over the last five years was weak. This was below our standards and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. RE/MAX’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.7% annually.

We can better understand the company’s revenue dynamics by analyzing its number of agents, which reached 146,627 in the latest quarter. Over the last two years, RE/MAX’s agents were flat. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, RE/MAX missed Wall Street’s estimates and reported a rather uninspiring 5.4% year-on-year revenue decline, generating $72.47 million of revenue. Company management is currently guiding for a 6.1% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.5% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

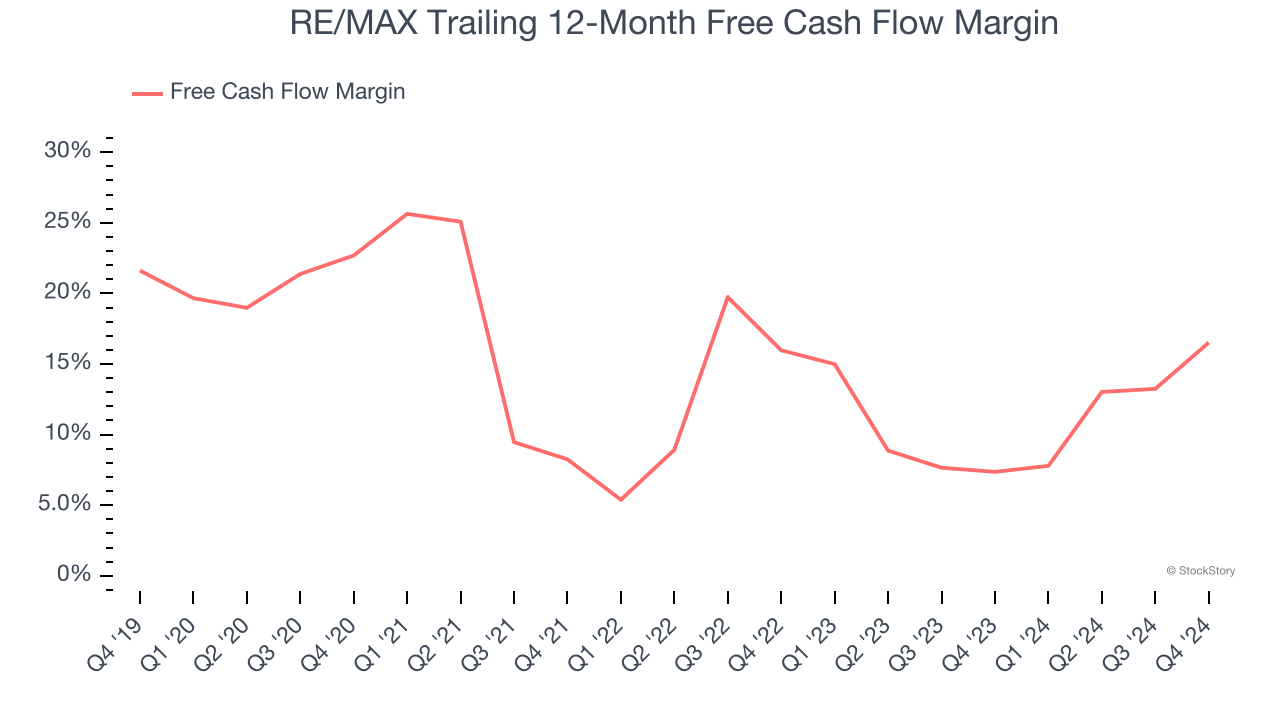

RE/MAX has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 11.8% over the last two years, slightly better than the broader consumer discretionary sector.

RE/MAX’s free cash flow clocked in at $15.98 million in Q4, equivalent to a 22.1% margin. This result was good as its margin was 13.6 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict RE/MAX’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 16.5% for the last 12 months will decrease to 3.1%.

Key Takeaways from RE/MAX’s Q4 Results

It was encouraging to see RE/MAX beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed significantly and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.1% to $10.01 immediately after reporting.

The latest quarter from RE/MAX’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.