Zumiez has been on fire lately. In the past six months alone, the company’s stock price has rocketed 88.7%, reaching $22.08 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Zumiez, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Do We Think Zumiez Will Underperform?

We’re happy investors have made money, but we're swiping left on Zumiez for now. Here are three reasons why ZUMZ doesn't excite us and a stock we'd rather own.

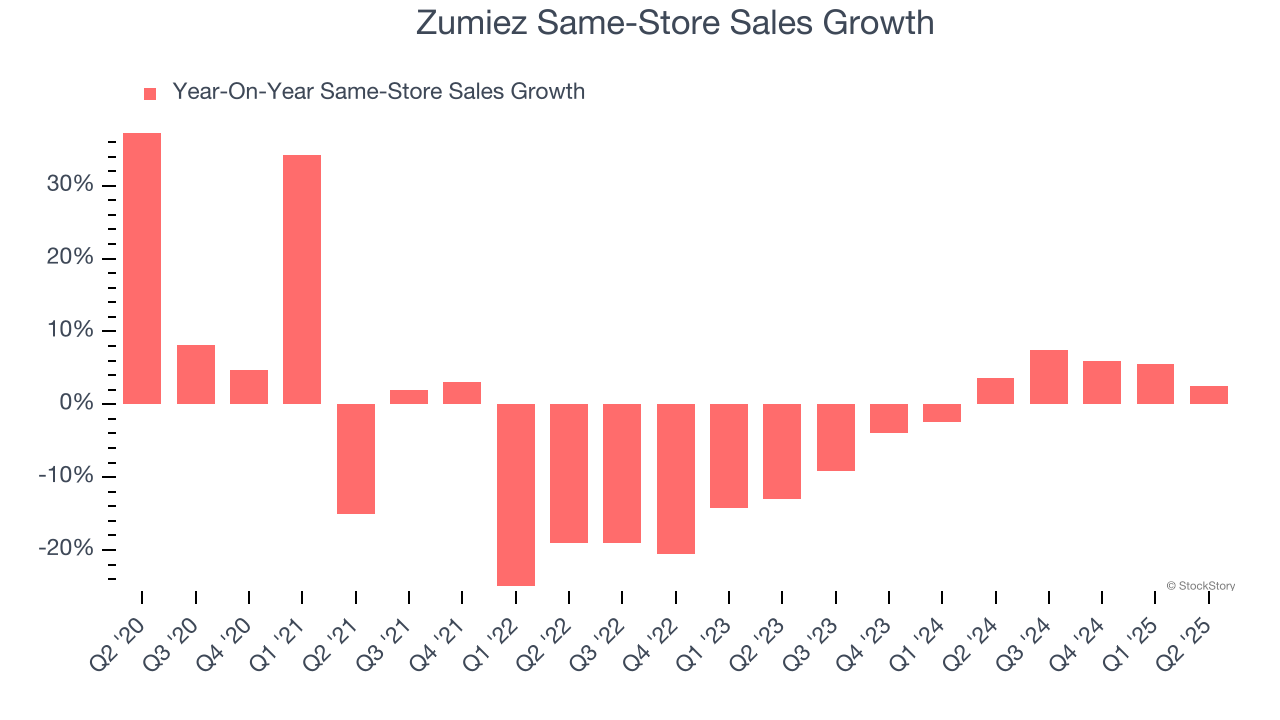

1. Same-Store Sales Falling Behind Peers

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Zumiez’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.2% per year.

2. Fewer Distribution Channels Limit its Ceiling

With $900.3 million in revenue over the past 12 months, Zumiez is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

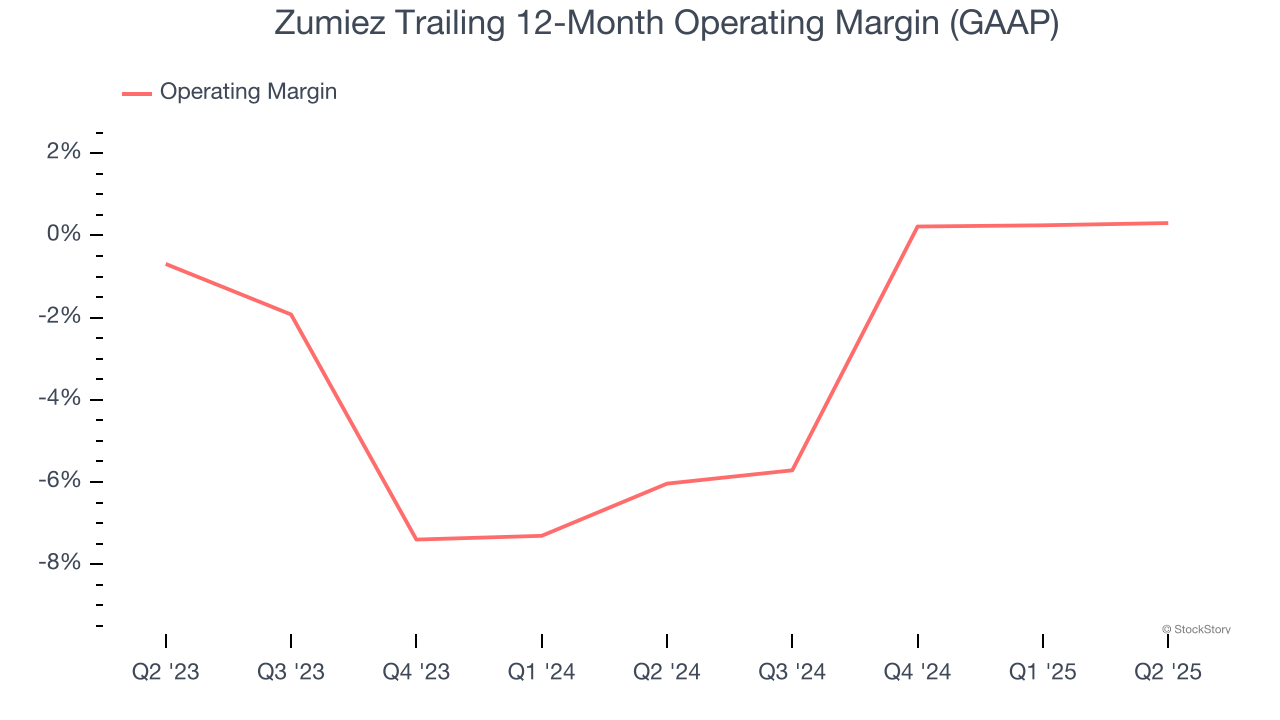

3. Operating Losses Sound the Alarms

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Although Zumiez broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 2.8% over the last two years. Despite the consumer retail industry’s secular decline, unprofitable public companies are few and far between. It’s unfortunate that Zumiez was one of them.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Zumiez, we’ll be cheering from the sidelines. Following the recent surge, the stock trades at 42.5× forward P/E (or $22.08 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

High-Quality Stocks for All Market Conditions

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.