What a fantastic six months it’s been for Lyft. Shares of the company have skyrocketed 60.1%, hitting $20.08. This run-up might have investors contemplating their next move.

Following the strength, is LYFT a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free for active Edge members.

Why Does LYFT Stock Spark Debate?

Founded by Logan Green and John Zimmer as a long-distance intercity carpooling company Zimride, Lyft (NASDAQ: LYFT) operates a ridesharing network in the US and Canada.

Two Things to Like:

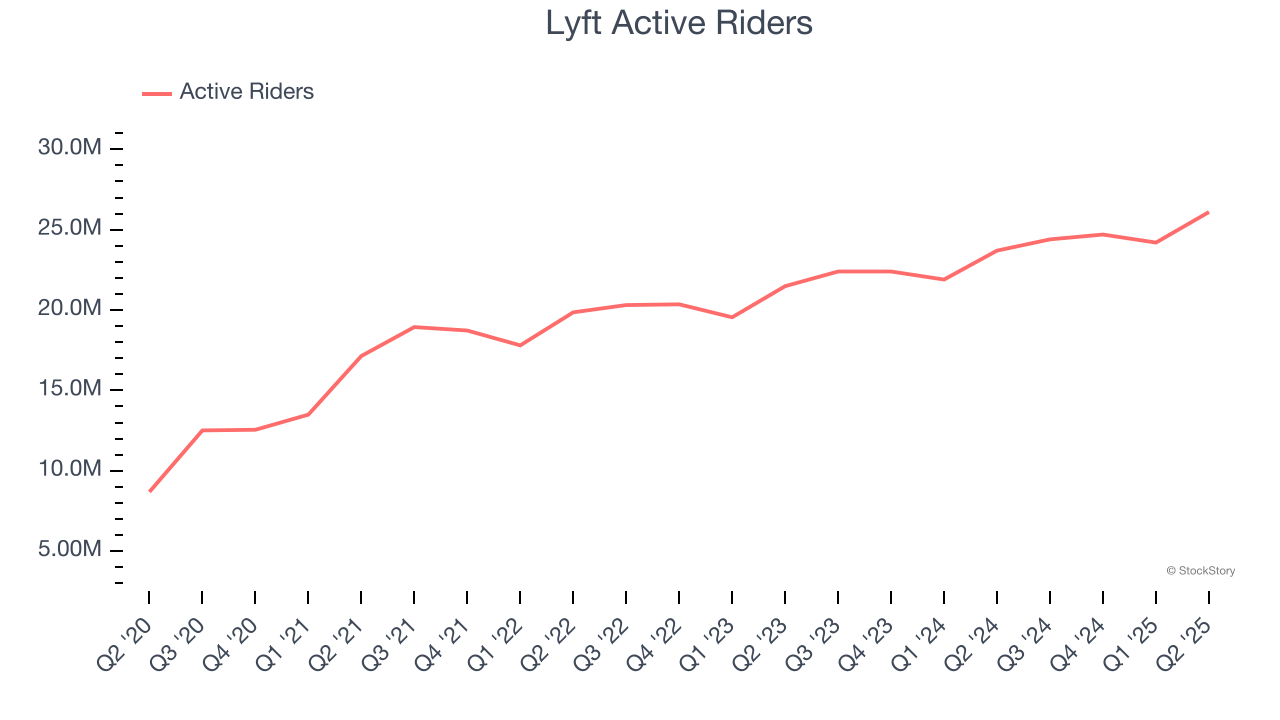

1. Active Riders Drive Additional Growth Opportunities

As a gig economy marketplace, Lyft generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, Lyft’s active riders, a key performance metric for the company, increased by 10.3% annually to 26.1 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

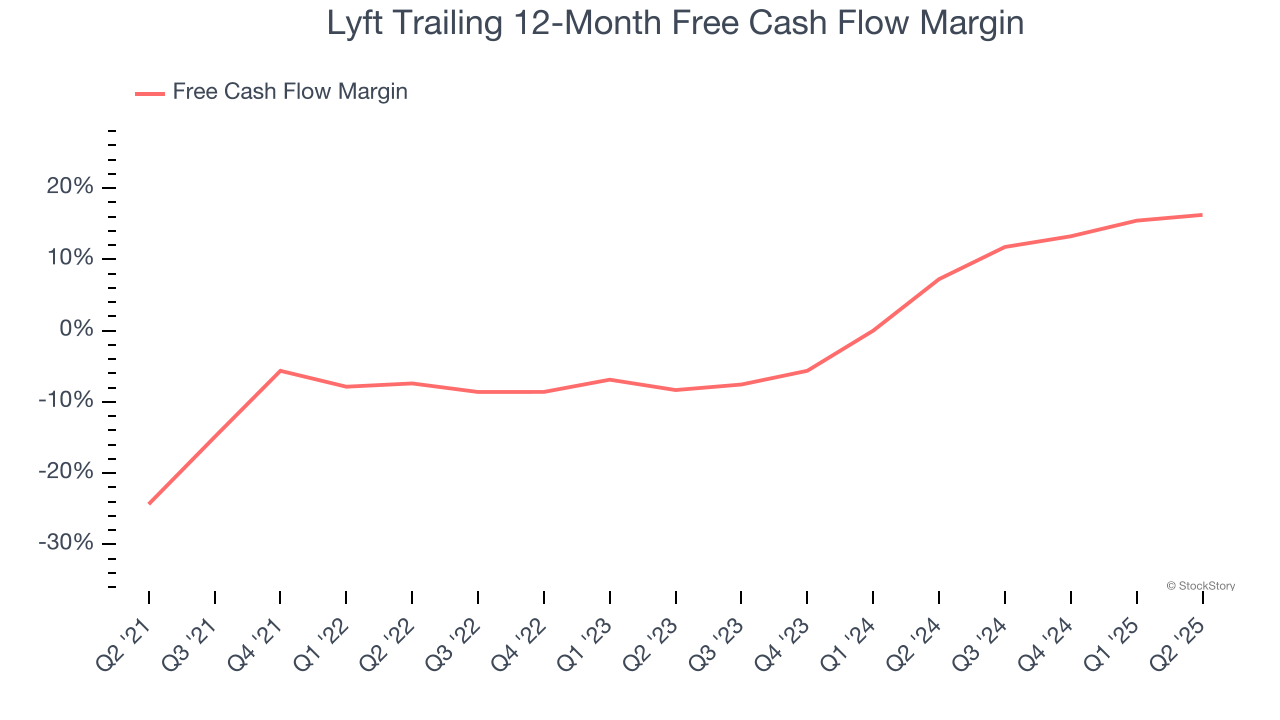

2. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Lyft’s margin expanded by 23.7 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Lyft’s free cash flow margin for the trailing 12 months was 16.2%.

One Reason to be Careful:

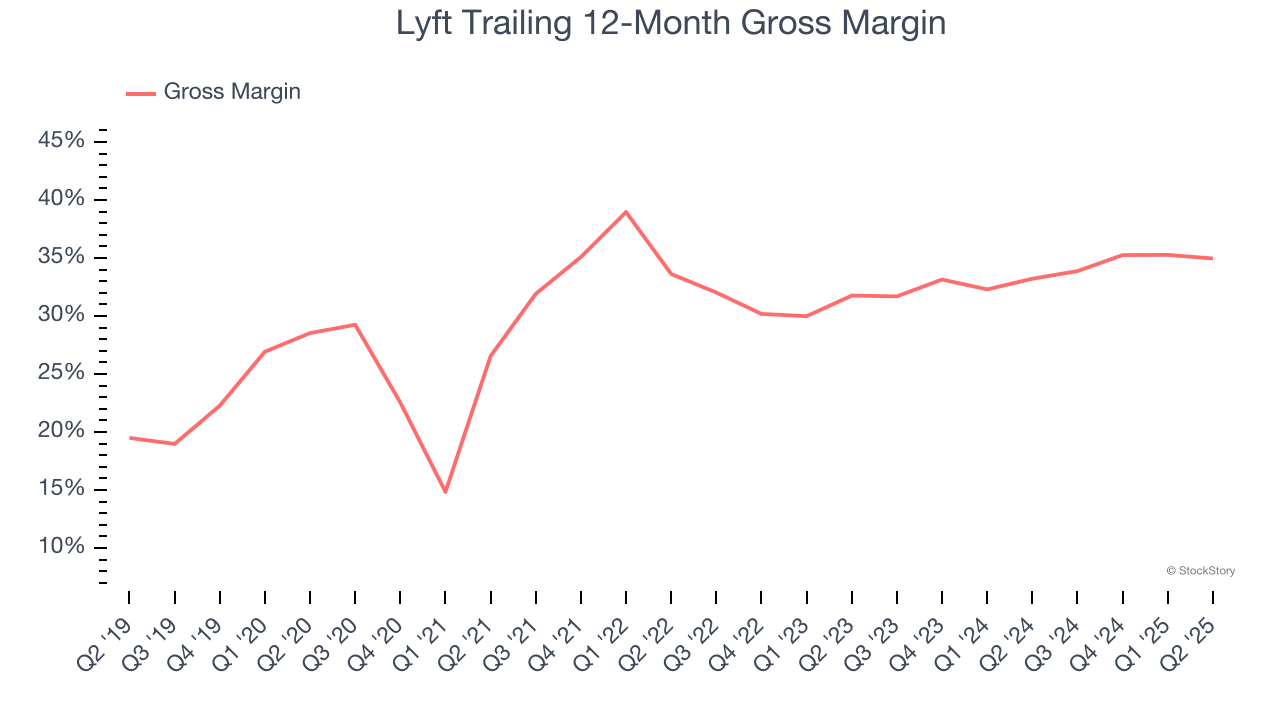

Low Gross Margin Reveals Weak Structural Profitability

For gig economy businesses like Lyft, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include server hosting, customer support, and payment processing fees. Another cost of revenue could also be insurance to protect against liabilities arising from providing transportation, housing, or freelance work services.

Lyft’s unit economics are far below other consumer internet companies, signaling it operates in a competitive market and must pay many third parties a slice of its sales to distribute its products and services. As you can see below, it averaged a 34.2% gross margin over the last two years. That means Lyft paid its providers a lot of money ($65.83 for every $100 in revenue) to run its business.

Final Judgment

Lyft’s merits more than compensate for its flaws, and after the recent rally, the stock trades at 14.6× forward EV/EBITDA (or $20.08 per share). Is now a good time to buy despite the apparent froth? See for yourself in our comprehensive research report, it’s free for active Edge members .

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.