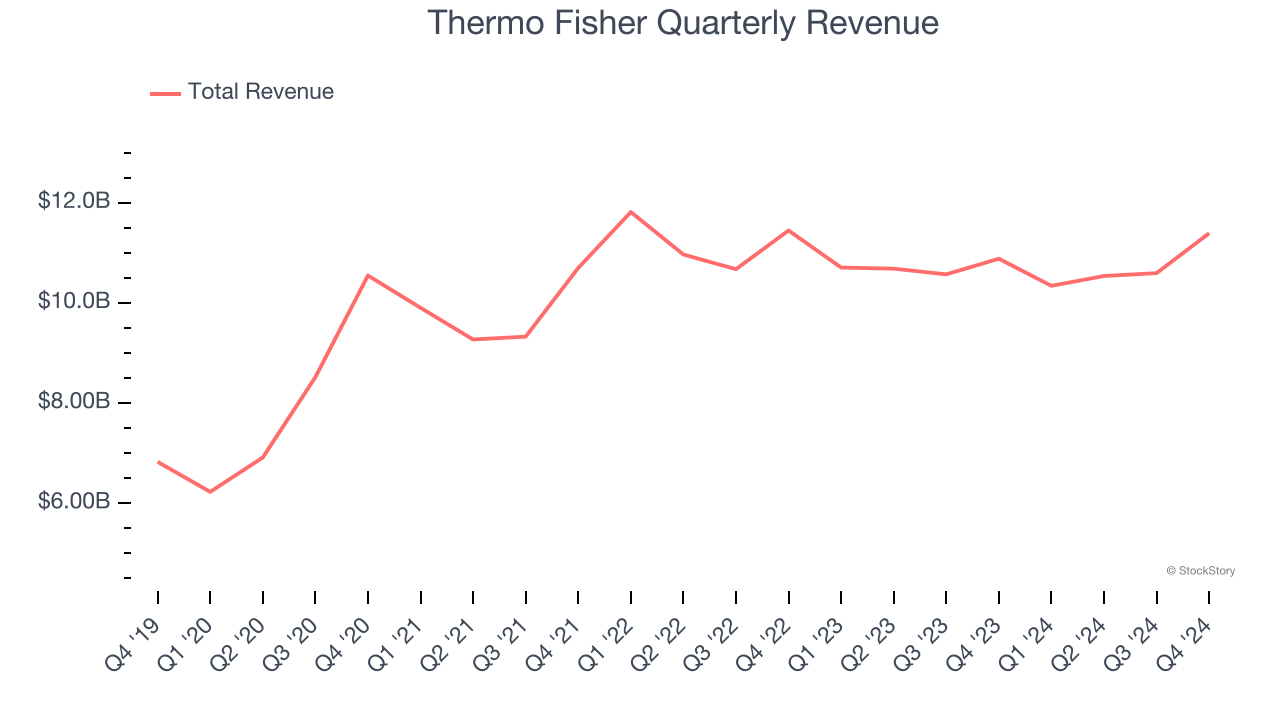

Life sciences company Thermo Fisher (NYSE: TMO) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 4.7% year on year to $11.4 billion. Its non-GAAP profit of $6.10 per share was 2.7% above analysts’ consensus estimates.

Is now the time to buy Thermo Fisher? Find out by accessing our full research report, it’s free.

Thermo Fisher (TMO) Q4 CY2024 Highlights:

- Revenue: $11.4 billion vs analyst estimates of $11.28 billion (4.7% year-on-year growth, 1% beat)

- Adjusted EPS: $6.10 vs analyst estimates of $5.94 (2.7% beat)

- Adjusted EBITDA: $2.76 billion vs analyst estimates of $2.95 billion (24.2% margin, 6.5% miss)

- Operating Margin: 17.7%, in line with the same quarter last year

- Free Cash Flow Margin: 24.7%, down from 30.5% in the same quarter last year

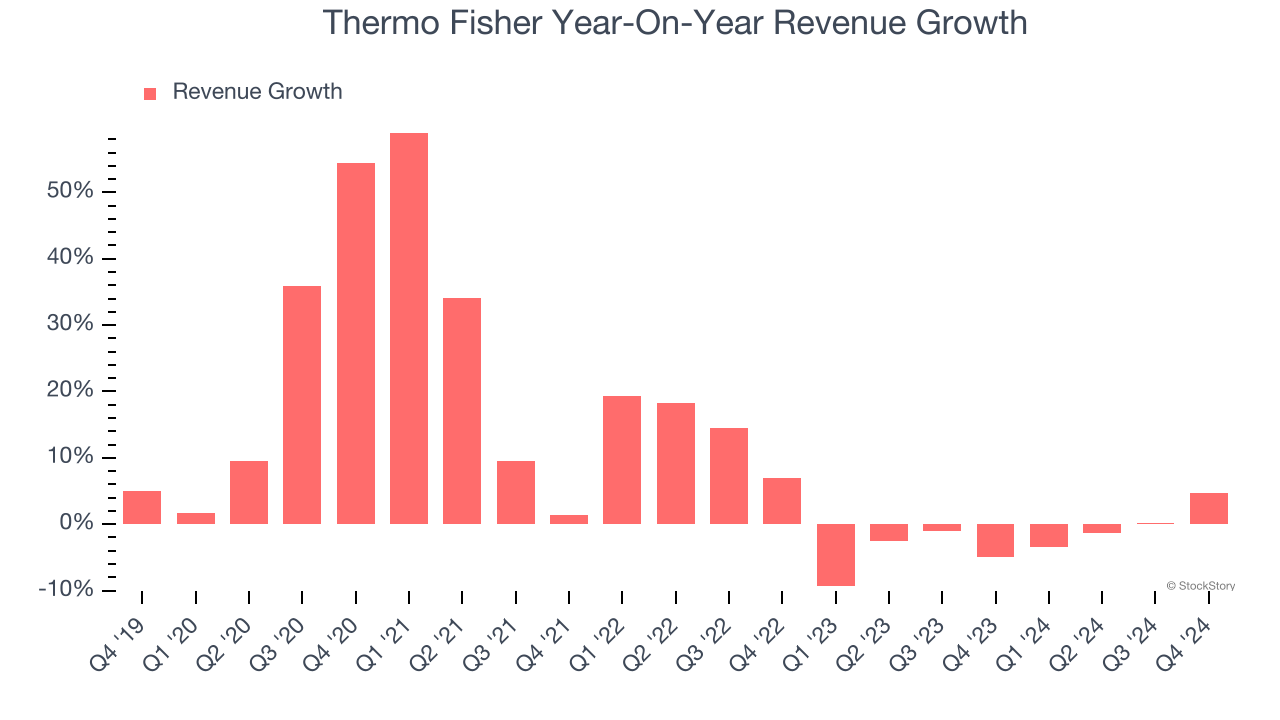

- Organic Revenue rose 4% year on year (-7% in the same quarter last year)

- Market Capitalization: $217.3 billion

“We finished 2024 with excellent financial performance, delivering strong growth on the top and bottom line in the fourth quarter,” said Marc N. Casper, Chairman, President and CEO of Thermo Fisher Scientific.

Company Overview

Known for their involvement in the Human Genome Project, Thermo Fisher (NYSE: TMO) supplies instruments, laboratory equipment, and reagents for scientific research and healthcare.

Research Tools & Consumables

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Thermo Fisher grew its sales at a decent 10.9% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Thermo Fisher’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 2.3% over the last two years.

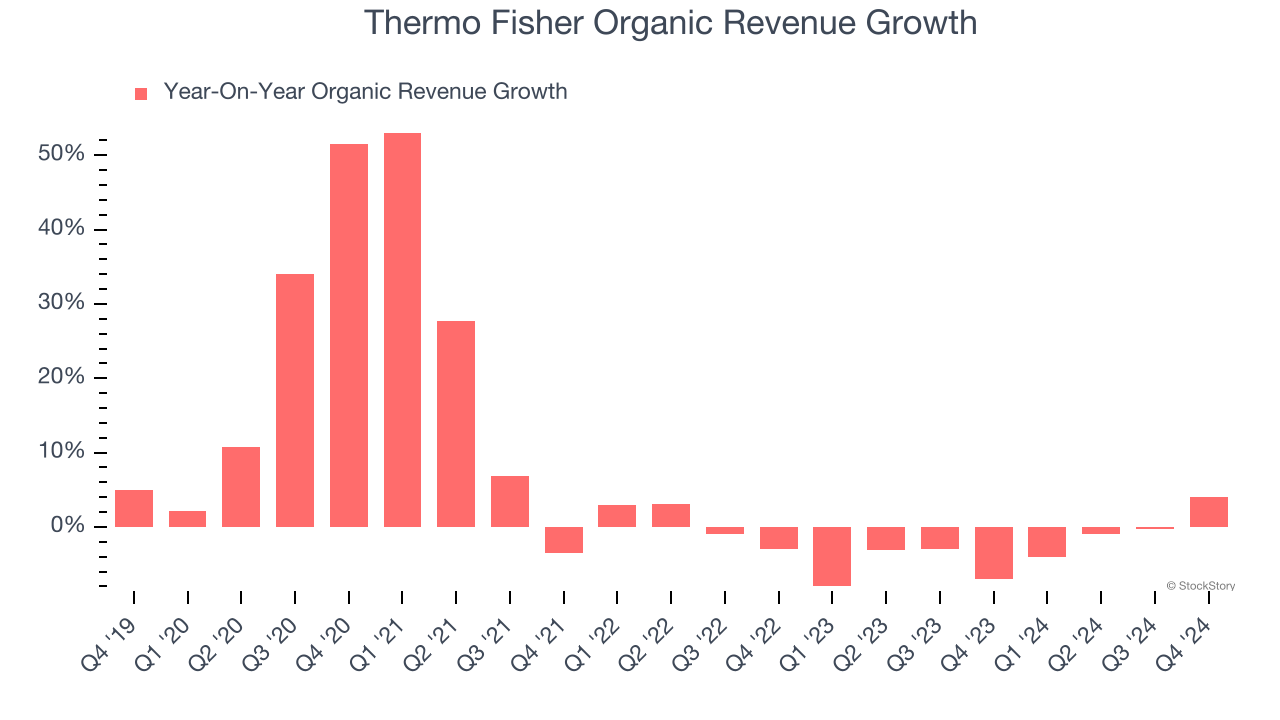

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don’t accurately reflect its fundamentals. Over the last two years, Thermo Fisher’s organic revenue averaged 2.8% year-on-year declines. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Thermo Fisher reported modest year-on-year revenue growth of 4.7% but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 3.7% over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

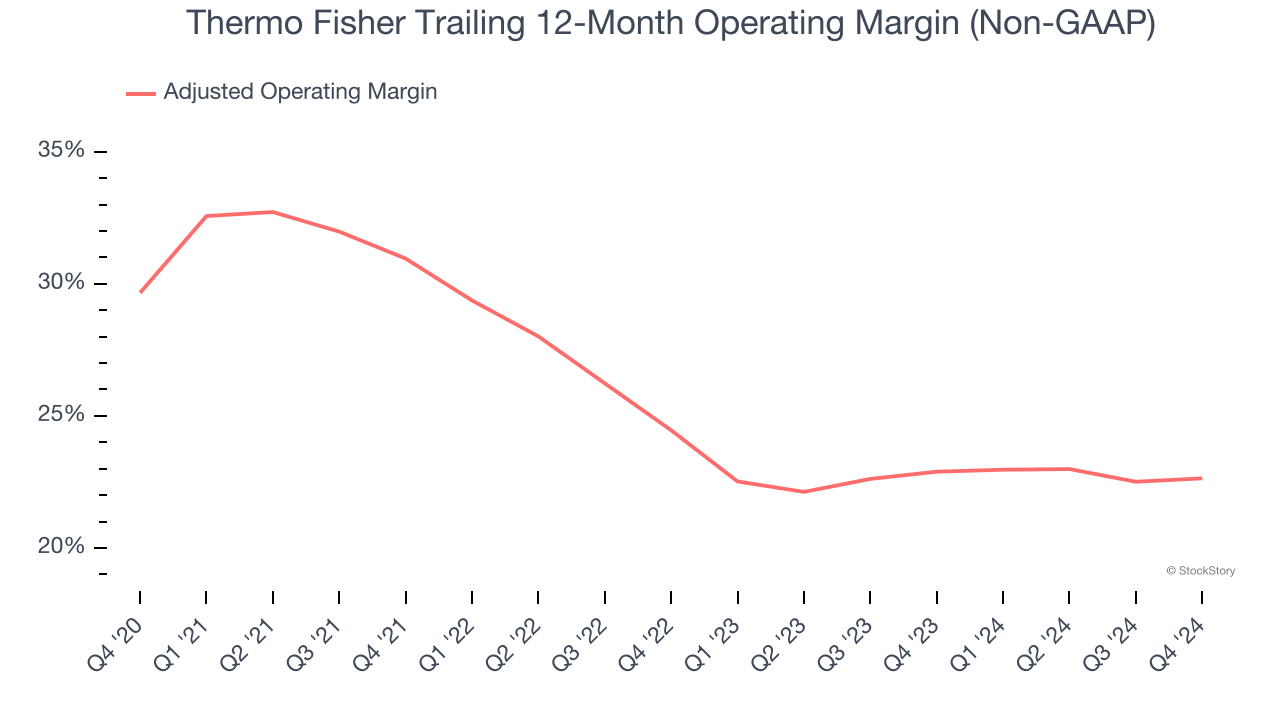

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Thermo Fisher has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 25.8%.

Looking at the trend in its profitability, Thermo Fisher’s adjusted operating margin decreased by 7 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 1.8 percentage points. This performance was poor no matter how you look at it - it shows operating expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Thermo Fisher generated an adjusted operating profit margin of 23.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

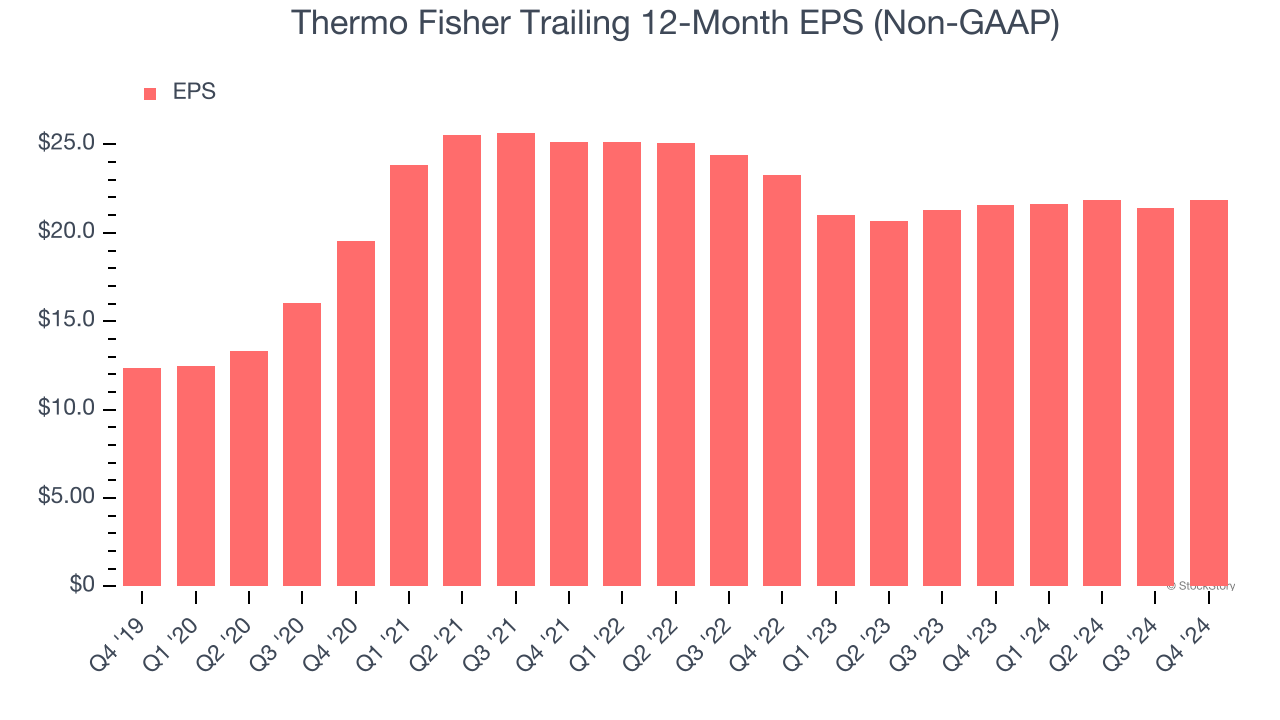

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Thermo Fisher’s EPS grew at a spectacular 12.1% compounded annual growth rate over the last five years, higher than its 10.9% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its adjusted operating margin didn’t expand.

We can take a deeper look into Thermo Fisher’s earnings quality to better understand the drivers of its performance. A five-year view shows that Thermo Fisher has repurchased its stock, shrinking its share count by 4.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Thermo Fisher reported EPS at $6.10, up from $5.67 in the same quarter last year. This print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects Thermo Fisher’s full-year EPS of $21.86 to grow 5.2%.

Key Takeaways from Thermo Fisher’s Q4 Results

It was good to see Thermo Fisher narrowly beat analysts’ organic revenue expectations this quarter. On the other hand, its operating income missed significantly and its EPS was in line with Wall Street’s estimates. Overall, this was a weaker quarter, but the stock traded up 6.9% to $606.98 immediately after reporting due to its top-line performance.

So should you invest in Thermo Fisher right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.