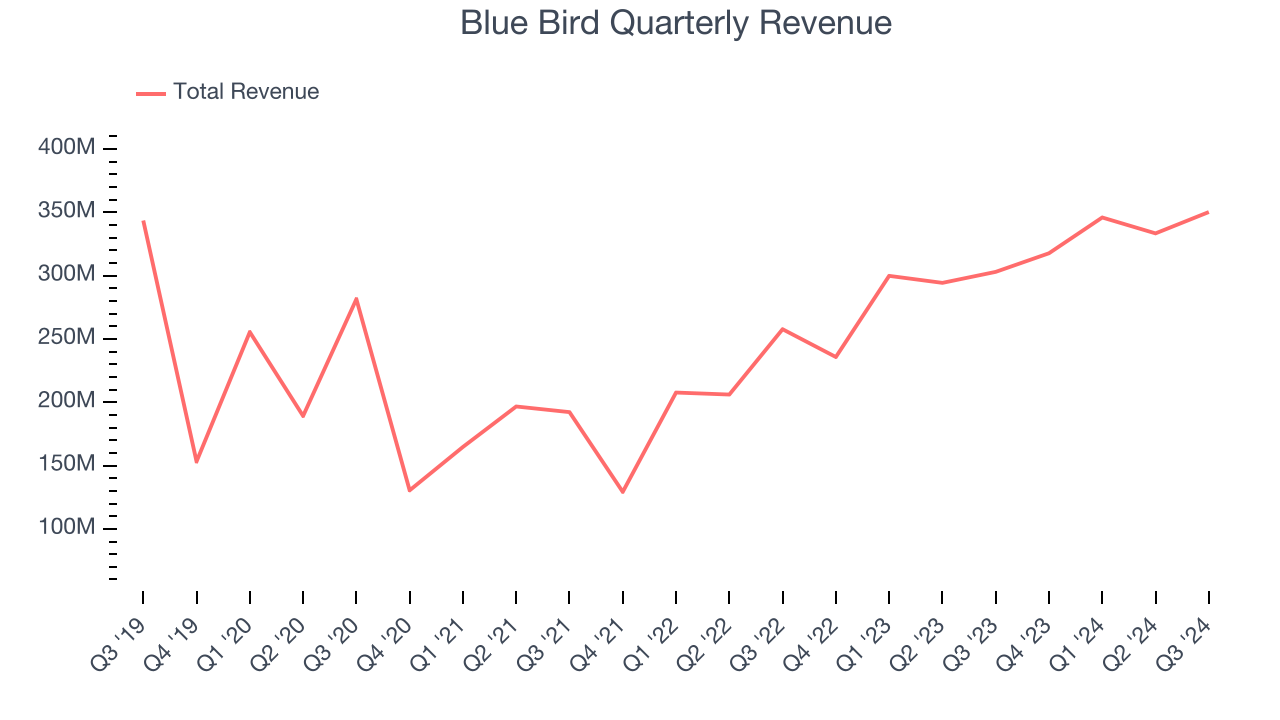

School bus company Blue Bird (NASDAQ: BLBD) reported Q3 CY2024 results exceeding the market’s revenue expectations, with sales up 15.6% year on year to $350.2 million. The company expects the full year’s revenue to be around $1.45 billion, close to analysts’ estimates. Its non-GAAP profit of $0.77 per share was 17.6% above analysts’ consensus estimates.

Is now the time to buy Blue Bird? Find out by accessing our full research report, it’s free.

Blue Bird (BLBD) Q3 CY2024 Highlights:

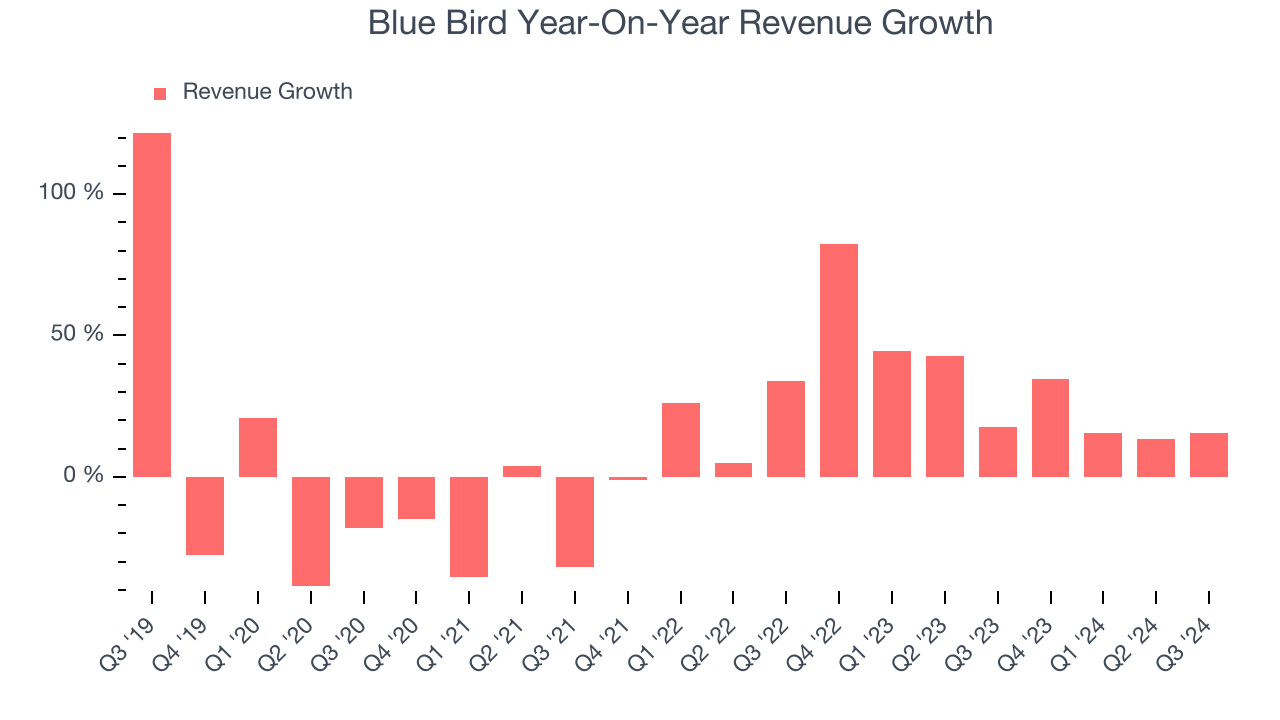

- Revenue: $350.2 million vs analyst estimates of $344 million (15.6% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.77 vs analyst estimates of $0.65 (17.6% beat)

- Adjusted EBITDA: $41.31 million vs analyst estimates of $36.05 million (11.8% margin, 14.6% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $1.45 billion at the midpoint, in line with analyst expectations and implying 7.6% growth (vs 19.8% in FY2024)

- EBITDA guidance for the upcoming financial year 2025 is $200 million at the midpoint, above analyst estimates of $191.1 million

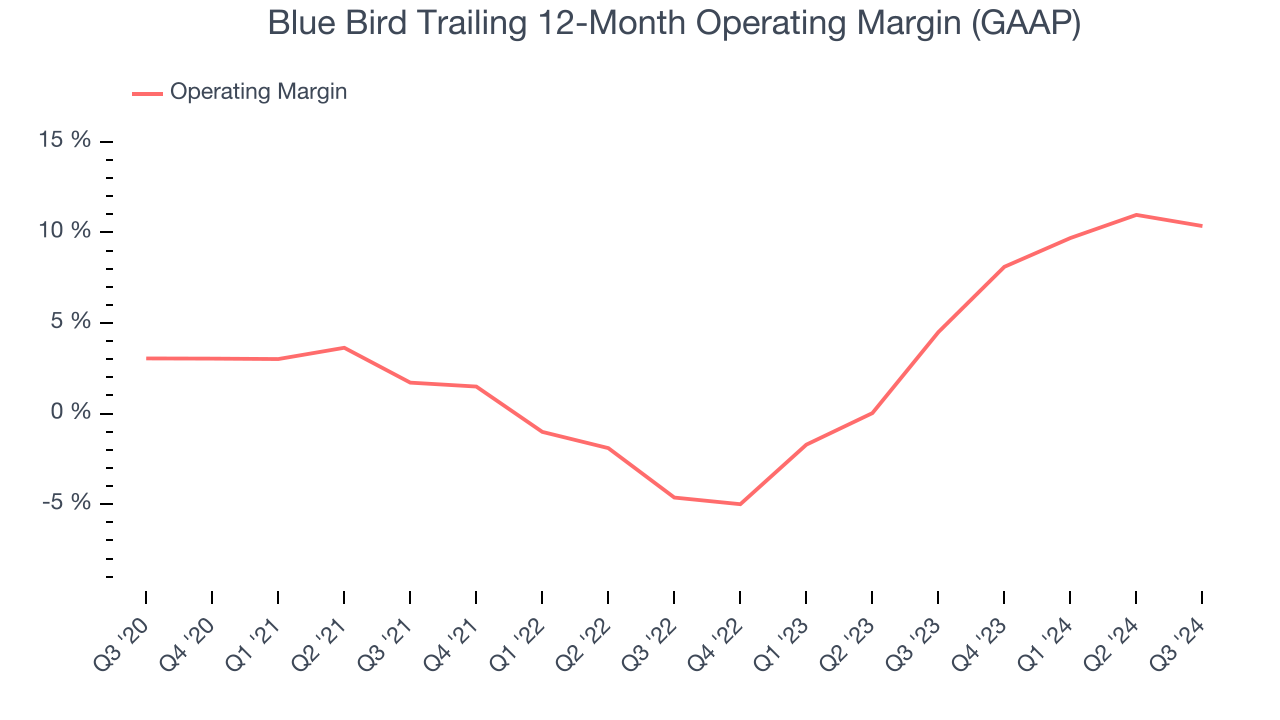

- Operating Margin: 7.3%, down from 9.5% in the same quarter last year

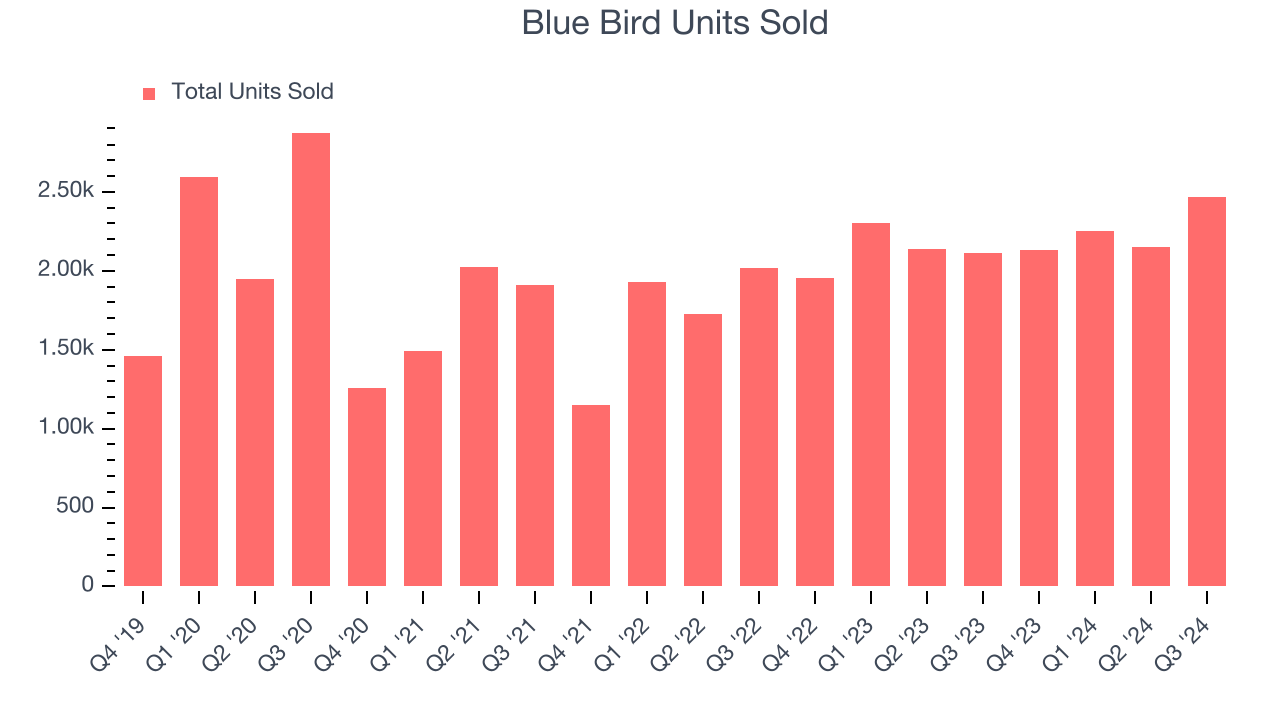

- Sales Volumes rose 16.5% year on year (5% in the same quarter last year)

- Market Capitalization: $1.33 billion

“I am incredibly proud of our team’s outstanding achievement in delivering a record profit in fiscal 2024, more than double last year’s then-record result,” said Phil Horlock, President & CEO of Blue Bird Corporation.

Company Overview

With around a century of experience, Blue Bird (NASDAQ: BLBD) is a manufacturer of school buses and complementary parts.

Heavy Transportation Equipment

Heavy transportation equipment companies are investing in automated vehicles that increase efficiencies and connected machinery that collects actionable data. Some are also developing electric vehicles and mobility solutions to address customers’ concerns about carbon emissions, creating new sales opportunities. Additionally, they are increasingly offering automated equipment that increases efficiencies and connected machinery that collects actionable data. On the other hand, heavy transportation equipment companies are at the whim of economic cycles. Interest rates, for example, can greatly impact the construction and transport volumes that drive demand for these companies’ offerings.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Blue Bird’s 4.6% annualized revenue growth over the last five years was tepid. This was below our standard for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Blue Bird’s annualized revenue growth of 29.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its units sold, which reached 2,466 in the latest quarter. Over the last two years, Blue Bird’s units sold averaged 17.8% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Blue Bird reported year-on-year revenue growth of 15.6%, and its $350.2 million of revenue exceeded Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow by 8.2% over the next 12 months. Still, this projection is above the sector average and suggests the market is factoring in some success for its newer products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Blue Bird was profitable over the last five years but held back by its large cost base. Its average operating margin of 4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Blue Bird’s operating margin rose by 7.3 percentage points over the last five years.

This quarter, Blue Bird generated an operating profit margin of 7.3%, down 2.2 percentage points year on year. Since Blue Bird’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

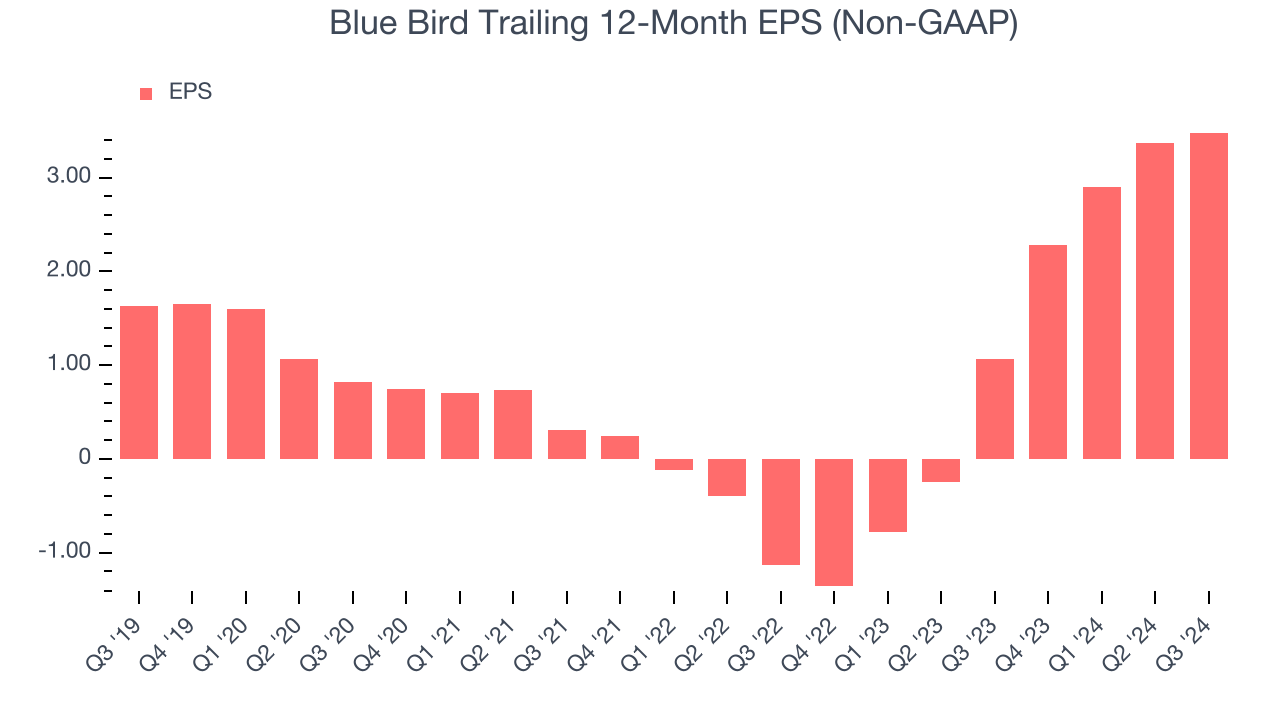

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Blue Bird’s EPS grew at a spectacular 16.4% compounded annual growth rate over the last five years, higher than its 4.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Blue Bird’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Blue Bird’s operating margin declined this quarter but expanded by 7.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Blue Bird, its two-year annual EPS growth of 125% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.In Q3, Blue Bird reported EPS at $0.77, up from $0.66 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Blue Bird’s full-year EPS of $3.48 to grow by 9.1%.

Key Takeaways from Blue Bird’s Q3 Results

We were impressed by how significantly Blue Bird blew past analysts’ sales volume expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year revenue guidance was in line. Zooming out, we think this was a solid quarter. The market seemed to focus on the negatives, and the stock traded down 4.8% to $41 immediately after reporting.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.