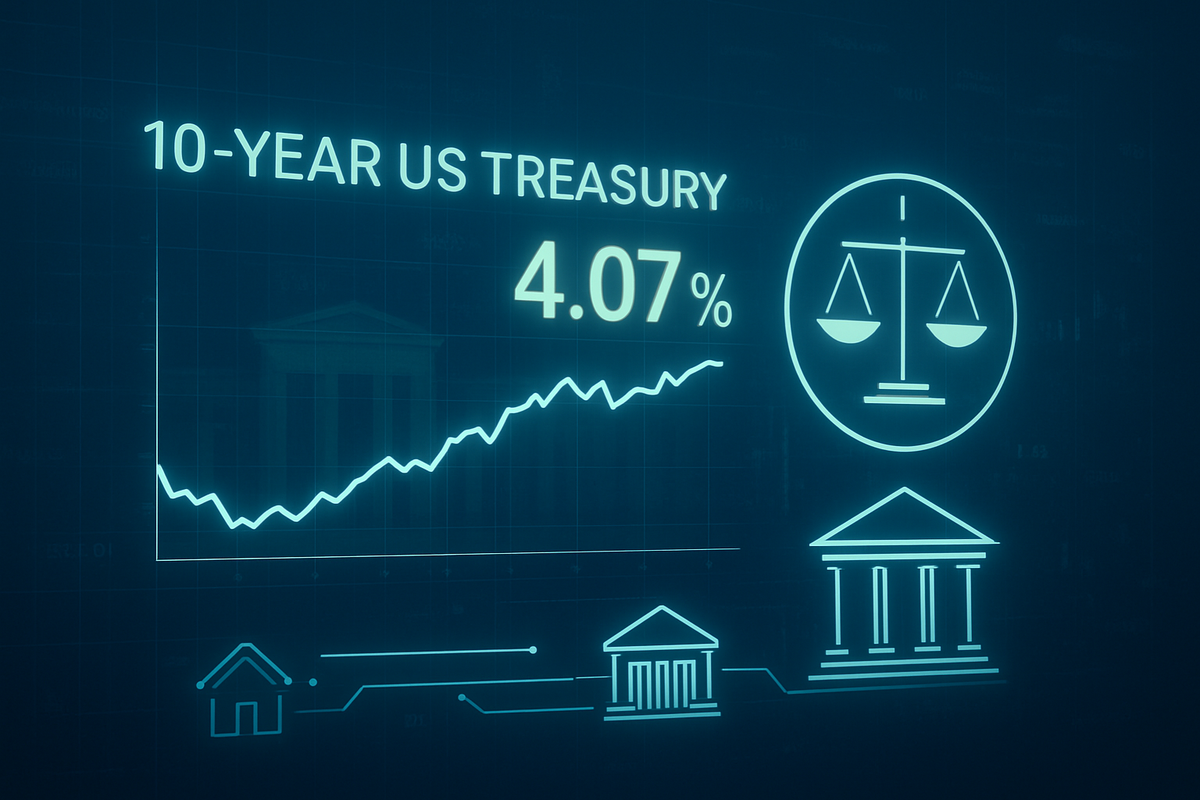

As of mid-February 2026, the pulse of the American economy is beating at a steady, if cautious, rhythm. The benchmark 10-year U.S. Treasury yield is currently hovering near 4.07%, a level that market analysts are calling a "hard-won equilibrium." This positioning reflects a delicate balancing act between cooling inflation data, which has finally begun to align with long-term targets, and a Federal Reserve that has shifted into a "wait-and-see" mode after a series of rate cuts in late 2025. For investors and consumers alike, this 4% threshold has become the new psychological and financial anchor for the mid-2020s.

The immediate implications of this yield stability are twofold: it provides a predictable floor for equity valuations, particularly in the technology sector, while simultaneously keeping borrowing costs high enough to remind the markets that the era of "easy money" is firmly in the rearview mirror. With the 10-year yield at 4.07%, the 30-year fixed mortgage rate has settled into a range between 6.09% and 6.20%. While this is a significant reprieve from the near-8% peaks seen in late 2023, it remains high enough to keep the "lock-in effect" alive in the housing market, as millions of homeowners continue to cling to pandemic-era mortgages sub-4%.

The Road to Equilibrium: A Timeline of the Fed’s Pivot

The current yield environment is the result of a programmatic shift in monetary policy that began in the final quarter of 2025. After maintaining restrictive rates for longer than many anticipated, the Federal Reserve executed three consecutive 25-basis-point cuts, bringing the federal funds rate to its current target range of 3.50%–3.75%. This transition was spurred by Core PCE inflation finally moderating to 2.4%, a level that gave Fed Chair Jerome Powell the confidence to signal that the central bank had reached "neutral territory"—a state where policy neither stimulates nor restricts economic growth.

The specific dip to 4.07% on the 10-year Treasury note occurred following the release of the January 2026 Consumer Price Index (CPI) data on February 13. The data showed headline inflation cooling faster than expected, prompting a brief rally in bonds. However, the Federal Open Market Committee (FOMC) has since doubled down on a "data-dependent" pause. Key players, including outgoing Chair Jerome Powell and his nominated successor, Kevin Warsh, have emphasized that while the "inflation panic" of the early 2020s has subsided, "sticky" service-sector costs and a resilient labor market (with unemployment steady at 4.4%) justify a cautious approach before any further easing.

Market reaction to this "wait-and-see" stance has been uncharacteristically calm. Unlike the volatility of 2024, the bond market in early 2026 is characterized by lower realized volatility. Institutional investors appear to have accepted that the Fed will likely remain on hold through at least the first half of the year. This stability has allowed the yield curve to begin a process of "un-inverting," a traditional signal that the economy is normalizing rather than heading toward a recessionary cliff.

Winners and Losers in the 4% Yield Era

The stabilization of yields at 4.07% has created a clear divide between sectors that can thrive in a "higher-for-longer" environment and those struggling under the weight of debt. Large-cap banking institutions, such as JPMorgan Chase & Co. (NYSE: JPM) and Bank of America Corp. (NYSE: BAC), are emerging as primary winners. These firms are benefiting from a steepening yield curve, which allows them to earn more on long-term loans while keeping deposit costs relatively stable, effectively expanding their Net Interest Margins (NIM).

In the technology sector, the stability of the 10-year yield is acting as a catalyst for continued investment in artificial intelligence. Companies like Microsoft Corp. (NASDAQ: MSFT) and NVIDIA Corp. (NASDAQ: NVDA) are utilizing their massive cash reserves and the predictable cost of capital to fund multi-billion dollar AI infrastructure projects. For these growth giants, a steady 4% yield is far more valuable than a volatile 3% yield, as it allows for more accurate long-term discounting of future cash flows and more confident capital allocation.

Conversely, the "losers" in this environment are primarily found in the commercial real estate sector and among highly leveraged "zombie" firms. 2026 is a "peak refinancing year," with over $1 trillion in corporate debt coming due. Companies that issued debt at 3% coupons during the pandemic are now facing a "refinancing shock" as they move to 5.5% or 6% rates. Real estate investment trusts (REITs) focused on office space, such as Vornado Realty Trust (NYSE: VNO), continue to face headwinds as high interest costs collide with lower occupancy rates, making it difficult to service existing debt loads.

The Broader Significance: AI Productivity vs. Fiscal Dominance

The current yield environment fits into a broader historical narrative of a "productivity-led soft landing." Unlike the stagflation fears of 2023, the 2026 economy is characterized by a significant uptick in productivity, largely attributed to the widespread integration of AI across the services and manufacturing sectors. This productivity boost allows for higher wages and a resilient GDP (currently forecasted at 2.3% for 2026) without the inflationary consequences that would typically follow, justifying the 10-year yield's position above 4%.

However, a shadow looms over this stability: fiscal dominance. The U.S. Treasury is tasked with managing a massive supply of debt, with an estimated $9.2 trillion in maturities occurring in 2026 alone. This high volume of supply exerts natural upward pressure on yields, regardless of Fed policy. Analysts point to this "supply overhang" as the primary reason why the 10-year yield has stayed above 4% even as inflation has neared the Fed's 2% target. It is a historical precedent rarely seen outside of wartime—high debt-to-GDP ratios requiring the market to demand a higher premium for holding sovereign debt.

The policy implications are significant. The Fed is no longer just fighting inflation; it is managing the liquidity of the Treasury market. If foreign demand for U.S. debt from central banks in Japan or China were to falter, the 10-year yield could spike regardless of what Jerome Powell says at the podium. This shift represents a transition from "monetary dominance," where the Fed dictates the economy, to "fiscal dominance," where the government's borrowing needs dictate the Fed's constraints.

Looking Ahead: The Warsh Transition and the 3.75% Threshold

As we move toward the second half of 2026, the market is laser-focused on two primary catalysts. The first is the leadership transition at the Federal Reserve. Kevin Warsh, known for a more hawkish lean during his previous tenure on the Board of Governors, is expected to take the helm in May 2026. Investors are closely watching his confirmation hearings for signs of whether he will prioritize the 2% inflation target at all costs or if he will tolerate slightly higher inflation to ensure the stability of the Treasury market.

The second catalyst is the "refinancing threshold." Mortgage analysts suggest that if the 10-year yield were to break below 3.75%, it would trigger a massive wave of refinancing activity. This would effectively act as a multi-billion dollar stimulus for the American middle class, potentially reigniting consumer spending. However, the Fed is wary of such a scenario, fearing it could lead to a "second wave" of inflation similar to the 1970s. Consequently, the Fed is likely to use its rhetoric to keep yields "anchored" near current levels for as long as the economy remains resilient.

In the short term, expect the 10-year yield to remain range-bound between 4.00% and 4.25%. A breach above 4.30% would likely signal a re-acceleration of inflation or a failed Treasury auction, while a drop below 3.90% would suggest the market is beginning to price in an economic slowdown that the Fed hasn't yet acknowledged.

Summary and Investor Outlook

The mid-February 2026 yield environment marks the end of the post-pandemic transition. The 4.07% yield on the 10-year Treasury represents a "new normal" where inflation is contained but interest rates remain meaningful. The key takeaway for investors is that the "Fed Put"—the idea that the central bank will aggressively cut rates at the first sign of market trouble—is significantly diminished by the reality of high federal debt and sticky service costs.

Moving forward, the market will be driven by earnings growth and productivity gains rather than multiple expansion fueled by falling rates. Investors should watch the quarterly Treasury Refunding Announcements as closely as they watch CPI data, as the supply of debt has become just as influential as the demand for it. The "Great Anchoring" of 2026 provides a stable backdrop, but the underlying pressures of fiscal spending and leadership changes at the Fed mean that this period of calm may be the eye of a very large, and very expensive, needle.

This content is intended for informational purposes only and is not financial advice.