As the 2025 holiday season reaches its peak, the global energy landscape is defined by a stark and unusual divergence. While crude oil prices have found a tenuous floor, remaining steady despite a backdrop of structural oversupply, natural gas prices are experiencing a sharp retreat. This "Great Energy Decoupling" reflects a market grappling with contradictory forces: record-breaking production levels in the Americas, unseasonably warm weather forecasts, and a corporate sector pivoting back to core hydrocarbon assets to fund the next generation of energy needs.

The immediate implications are significant for both consumers and investors. For the first time in years, the historical correlation between oil and gas has weakened. Crude is locked in a "bearish stability," hovering at four-year lows but refusing to break further due to persistent geopolitical friction. Meanwhile, natural gas—which began December with a bullish surge—has seen its gains evaporated by a mid-month "weather wipeout," signaling that even record-high export capacity cannot fully insulate the commodity from the volatility of a warming climate.

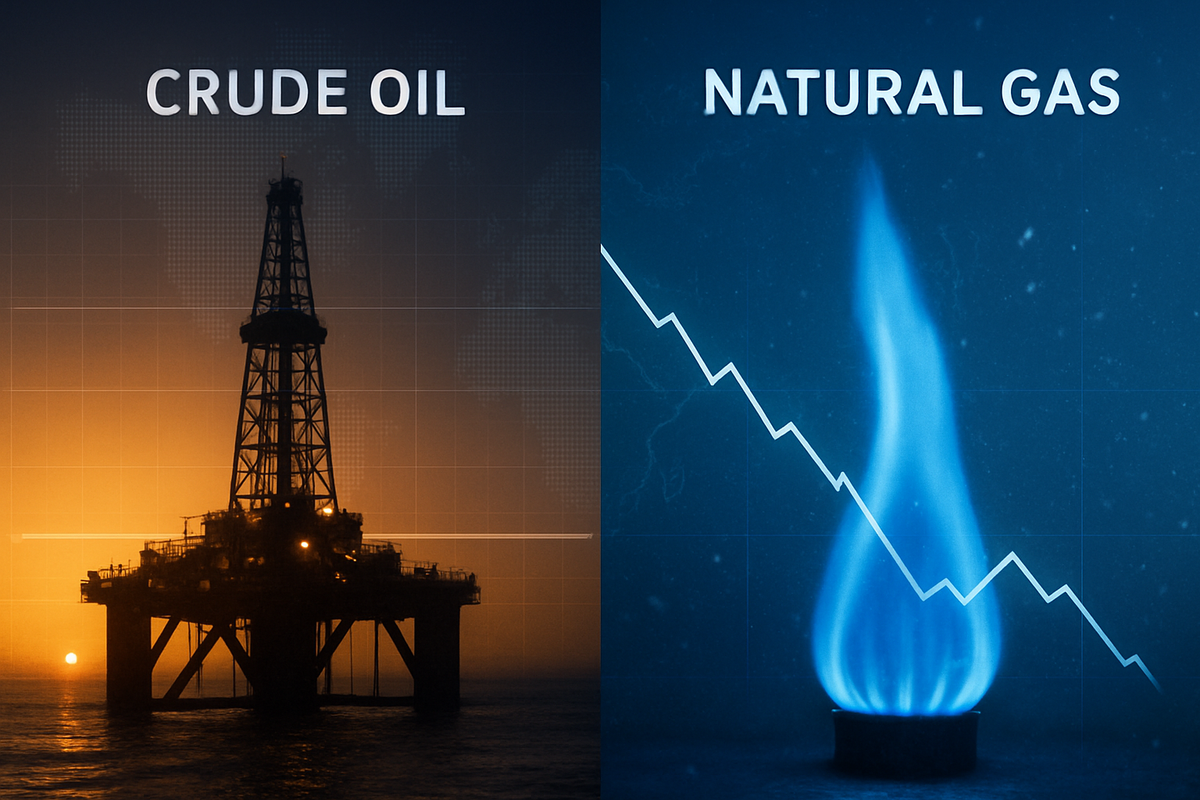

A Tale of Two Commodities: The December Divergence

The closing weeks of 2025 have seen West Texas Intermediate (WTI) crude settle into a narrow range between $58 and $60 per barrel, while Brent crude has anchored near $62. This stability is not a sign of market strength but rather a stalemate between massive supply and fragile demand. The United States has solidified its position as the world’s leading producer, maintaining a record output of 13.6 million barrels per day. This surge, combined with significant capacity additions from Guyana and Brazil, has effectively neutralized the production cuts previously implemented by OPEC+. By late December, the cartel began a phased unwinding of these cuts to reclaim lost market share, further saturating an already well-supplied market.

In contrast, the natural gas market has been a theater of volatility. After peaking above $5.00/MMBtu at the Henry Hub during an early December cold snap, prices slid roughly 25% to settle between $3.94 and $4.40/MMBtu by December 24. The primary catalyst for this slide was a dramatic shift in meteorological models predicting unseasonably mild temperatures across the U.S. and Europe for the remainder of the year. This dampened the immediate demand for heating, leaving regional storage levels—particularly in the European Union—at a healthy 70-72% capacity.

The timeline of this divergence was accelerated by mid-month rumors of potential peace negotiations in the Russia-Ukraine conflict. On December 15, reports of a diplomatic breakthrough caused a rapid compression of the "geopolitical risk premium," triggering a 2.7% single-day drop in oil prices. However, while oil stayed down, natural gas remained tethered to the weather, failing to recover even as the U.S. government rushed to expedite new LNG export licenses under the latest "Liberation Day" trade policies.

Corporate Maneuvers: BP’s Strategic Pivot and the Castrol Sale

The corporate world is responding to these shifting dynamics with aggressive portfolio restructuring. A standout event this month was the announcement from BP (NYSE: BP) regarding the sale of its 65% stake in Castrol to the investment firm Stonepeak. The deal, valued at an enterprise value of $10.1 billion, provides BP with approximately $6 billion in net proceeds. This move is a cornerstone of BP’s "Return to Core" strategy, as the company seeks to simplify its operations and reduce its net debt to a target of $14–$18 billion by 2027.

The impact was felt immediately in international markets. Castrol India (NSE: CASTROLIND), a publicly listed subsidiary, saw its share price jump nearly 9% on December 24 following the news. Under SEBI regulations, the change in global ownership triggered a mandatory open offer for public shareholders, creating a liquidity event that investors eagerly anticipated. While BP divests from downstream lubricants, it is doubling down on high-margin integrated hydrocarbons and the burgeoning power demands of the AI and data center revolution.

Other major players are also feeling the heat. Companies heavily weighted toward natural gas production, such as EQT Corporation (NYSE: EQT) and Chesapeake Energy (NASDAQ: CHK), are facing margin pressure from the recent price slide. Conversely, diversified giants like ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) are benefiting from their massive U.S. shale footprints, which allow them to remain profitable even at $60 oil, thanks to lower extraction costs and integrated refining operations that capitalize on cheaper feedstock.

Wider Significance: The AI Power Surge and Geopolitical Shifts

The divergence in 2025 is more than just a seasonal anomaly; it fits into a broader trend where natural gas is being repositioned as a "bridge fuel" for the digital age. The rapid expansion of AI data centers has created an insatiable demand for reliable, 24/7 baseload power, a role that natural gas is increasingly filling as coal plants are retired and nuclear projects face long lead times. This structural demand provides a long-term bullish narrative for gas that contrasts sharply with the "peak oil" concerns dogging the crude market.

Furthermore, the geopolitical landscape is shifting. The implementation of new U.S. trade tariffs in late 2025 has created a bearish environment for global crude trade by threatening to slow industrial activity. However, these same policies have been bullish for domestic gas infrastructure, as the administration views LNG exports as a critical tool for energy diplomacy and economic leverage. This has led to a record 18 Bcf/d in U.S. LNG exports, linking domestic Henry Hub prices more closely to global demand than ever before.

Historically, this period mirrors the energy market of the mid-2010s, but with a twist. While the previous decade was defined by the "shale gale," the current era is defined by "efficiency and export." The industry has learned to produce more with less, and the ability to move that product globally via LNG tankers or pipelines has fundamentally changed the price discovery mechanism for natural gas, making it more sensitive to global economic shifts and less to local supply gluts.

Looking Ahead: Strategic Pivots in a Low-Price Environment

In the short term, the energy sector will remain highly sensitive to weather patterns. Should a "polar vortex" emerge in January 2026, natural gas prices could see a violent reversal, potentially reclaiming the $5.00 mark. However, the long-term outlook for crude remains challenged. With global demand growth slowing to just 0.7 million barrels per day—largely due to China’s industrial cooling and the accelerating adoption of electric vehicles—oil producers will need to find new ways to maintain profitability.

Market opportunities are likely to emerge in the infrastructure and midstream sectors. As the U.S. continues to push its "energy liberation" agenda, companies involved in pipeline expansion and LNG terminal construction will be well-positioned. For producers, the strategic pivot will involve a transition from volume growth to value return. We expect to see more "Return to Core" divestments similar to the BP-Castrol deal, as companies prune non-essential assets to focus on the most efficient acreage in the Permian Basin and other low-cost regions.

Conclusion: Investors Should Watch the Weather and the Wells

The divergence of late 2025 serves as a reminder that the energy market is no longer a monolithic entity. Crude oil is entering a period of structural surplus, where geopolitical "black swans" are the only thing preventing a deeper price collapse. Natural gas, while currently sliding due to a warm winter, is becoming the backbone of the global power grid and a key export commodity, subject to both the whims of the weather and the demands of the AI sector.

For investors, the key takeaways are clear: watch the inventory levels in Europe and the production reports from the U.S. Permian Basin. The BP-Castrol deal highlights a trend of corporate consolidation and debt reduction that will likely continue through 2026. As we move into the new year, the ability to distinguish between seasonal volatility and structural shifts will be the difference between capturing gains and being caught in the slide.

This content is intended for informational purposes only and is not financial advice.