It’s not often that we find high dividend stocks that also offer significant upside potential. However, Accenture (ACN) would fit the bill after falling over 45% from its all-time highs. The stock not only has a dividend yield of 3.1%, which is over twice the S&P 500 Index’s ($SPX) yield, but the average sell-side analyst sees it rising to $295.35 over the next year, which is 43% higher than current levels. Let's explore whether it makes sense to add ACN stock after the recent crash. We'll begin by analyzing why the stock has fallen in the first place.

Why Has Accenture Stock Dropped?

There are two key reasons why Accenture stock has dropped sharply over the last year. Firstly, discretionary client spending has been cautious, and it did not help that Accenture lost federal contracts last year as part of the Donald Trump administration’s cost-cutting under the Elon Musk-headed Department of Government Efficiency (DOGE).

Then there is the question of the very business model of companies like Accenture amid fears that artificial intelligence (AI) might cannibalize traditional consulting and IT services. With AI looking to automate coding and back-office tasks, the "man-hours" model that firms like Accenture rely on could be at risk. The flurry of AI tools released by Anthropic particularly compounded such fears and led to a selloff in software stocks.

Accenture's AI-Powered Rebound

Meanwhile, even as AI is seen as an existential threat to companies like Accenture, the management thinks otherwise and believes that AI can actually help it grow its business. The company has seen strong growth in advanced AI business booking, and the metric doubled on an annual basis to $2.2 billion in fiscal Q1 2026.

While an increasing number of companies are looking to adopt AI, they would also need consulting and professional services companies (like Accenture) to implement these projects. Unlike consumer AI, where adoption can be instant and seamless, in enterprise AI, companies must consider several factors, including the safety of the massive data they handle and the long-term payoffs. As CEO Julie Sweet put it during the fiscal Q1 earnings call, “Clients increasingly understand that advanced AI is not a quick fix. Adopting it successfully requires foundational work to deliver P&L impact and other critical outcomes.”

Accenture has made acquisitions in the AI space, which help enhance its capabilities and increase its target market. Also, the company has been training its workforce in AI and has been pretty clear in its communication that those who cannot be reskilled will be laid off, while senior employees will lose out on promotion unless they use AI tools.

Incidentally, when it comes to execution, Accenture has fared better than many of its peers and has gained market share in the consulting and IT services industry. It also saw margin expansion in the most recent quarter as revenue growth outstripped headcount growth.

ACN Stock Looks Too Cheap to Ignore Now

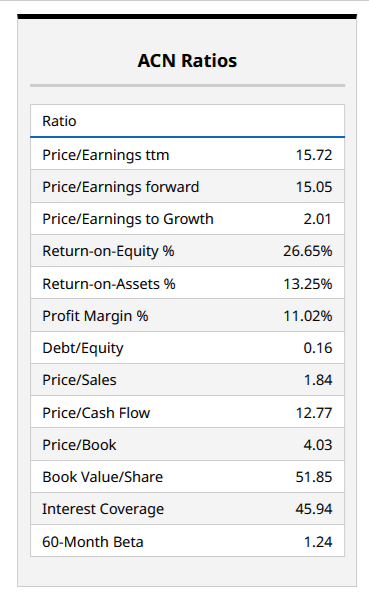

ACN stock trades at a forward price-to-earnings (P/E) multiple of just about 15x, while the price-to-cash flow multiple is 12.77x. Both these multiples look quite attractive, and the depressed valuations suggest that markets don’t believe that Accenture can turn AI into an opportunity.

However, I find the stock’s valuations quite reasonable here and believe the AI fears are overblown, especially with Accenture positioning itself for the expected increase in AI deployments by its customers. By proactively retraining its workforce in AI, Accenture has positioned itself well for the AI era and laid the groundwork for long-term growth.

Accenture’s Dividend Yield of Over 3%

Along with the capital appreciation, investors can also expect a healthy dividend from Accenture. Last year, the company raised its quarterly dividend by 10.1% to $1.63 per share, which represents a dividend yield of over 3.1% at current prices. The company’s dividends have grown at an annualized rate of 10.7% since 2019, when it moved to a quarterly dividend from the existing policy of half-yearly dividends.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend Stock Yields 3.1% and Offers Massive Upside: Time to Buy?

- SoundHound Is One of the Most Short Stocks Right Now. Should You Bet on a SOUN Squeeze?

- Down 15% in 2026, Should You Buy the Dip in Microsoft Stock?

- 1 ‘Strong Buy’ AI Stock That Wedbush Loves Now: ‘No Lost Deals’ Amid ‘Disruption’