Investors in defense giant RTX Corporation (RTX) may want to circle Mar. 6 on their calendars. The White House is preparing to host top executives from America’s largest weapons manufacturers, including RTX, for an urgent meeting aimed at accelerating weapons production as U.S. munitions stockpiles shrink amid escalating conflict with Iran.

The gathering comes as the Pentagon grapples with rapidly depleting inventories after intensive military operations, including the recent U.S.-Israel strikes on Iranian targets and continued support for conflicts in the Middle East. Officials are increasingly concerned that missile interceptors, artillery shells, and other critical munitions are being consumed faster than they can be replenished.

For investors, the implications could be significant. While Donald Trump said the U.S. has a “virtually unlimited supply” of munitions, the U.S. government is reportedly considering a supplemental defense package of roughly $50 billion to replenish weapons and ramp up production capacity, potentially creating a surge in demand for systems produced by companies like RTX, which manufactures key missile and defense technologies.

Meanwhile, defense companies have already begun increasing output, with RTX aiming to eventually increase Tomahawk missile production to 1,000 units annually.

Thus, this White House meeting could mark a pivotal moment for the defense industry and for RTX shareholders. And, it might trigger the next wave of defense spending tied to the widening Iran conflict.

About RTX Corporation Stock

RTX Corporation is an aerospace and defense company headquartered in Arlington, Virginia. Formed in 2020 through the merger of Raytheon Company and United Technologies and formerly known as Raytheon Technologies, the company develops advanced aircraft engines, missile systems, avionics, sensors, and defense technologies for commercial and military customers worldwide. RTX operates through three major divisions: Collins Aerospace, Pratt & Whitney, and Raytheon, serving both the global aerospace industry and government defense programs. The company is one of the largest defense contractors in the world and has a market cap of $280.3 billion.

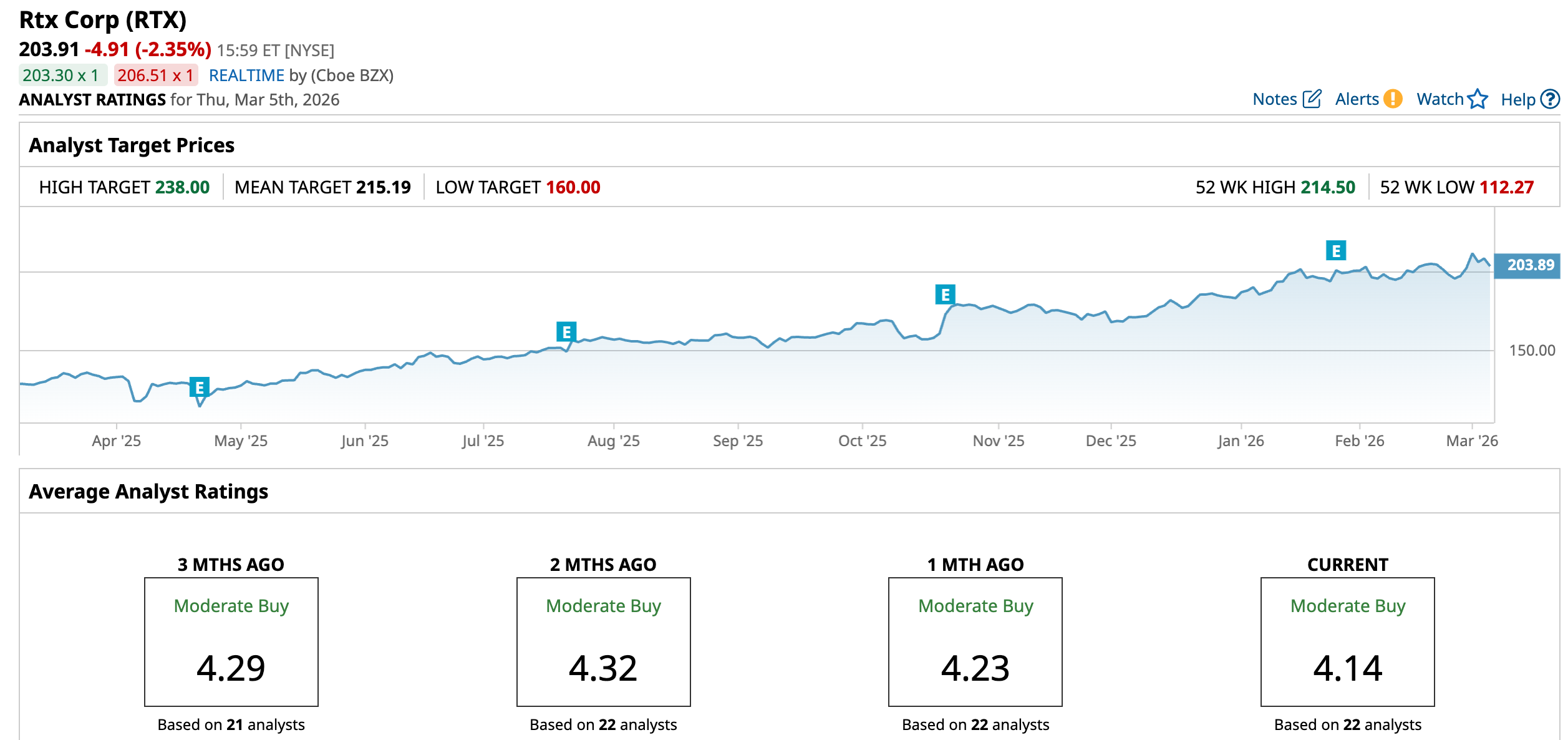

Shares of RTX Corporation have delivered a strong rally over the past year, significantly outperforming the broader market. The aerospace and defense giant’s stock has surged 56.5% over the past 52 weeks, amid robust demand for military systems, improving earnings momentum, and rising global defense spending. And year-to-date (YTD), the stock has climbed about 10.63%, extending last year’s powerful rally and trading near recent highs.

More recently, geopolitical tensions have provided an additional catalyst. RTX has surged after the escalation of the U.S.-Israel war with Iran, with shares hitting new highs as investors priced in expectations for increased weapons demand and higher defense spending. The stock is just 5% below its multi-year high of $214.50, reached on Mar. 3.

The rally underscores how RTX is increasingly viewed by investors as a geopolitical hedge, benefiting from rising global security concerns and the potential for accelerated missile and munitions production as the U.S. moves to replenish depleted stockpiles.

The stock is currently trading at a premium valuation compared to industry peers, at 30.33 times forward earnings.

Strong Financial Performance

RTX Corporation released its fourth-quarter and full-year 2025 results on Jan. 27.

For the quarter ended December 2025, RTX reported sales of $24.24 billion, representing a 12% year-over-year (YOY) increase. Adjusted earnings per share (EPS) came in at $1.55, slightly higher than the $1.54 reported a year earlier, and above the consensus estimate. Importantly, the company generated $4.2 billion in operating cash flow, translating into free cash flow of $3.2 billion, a dramatic improvement compared with $492 million in free cash flow in Q4 2024, highlighting a sharp recovery in cash generation. RTX also ended the year with a solid backlog of $268 billion, underscoring strong long-term demand for its aircraft engines, avionics, and missile systems.

For the full fiscal year, RTX delivered $88.6 billion in revenue, representing 10% YOY growth. Its adjusted EPS increased to $6.29, up 10% YOY from $5.73. The company also significantly strengthened its cash generation, with free cash flow climbing to $7.9 billion, an increase of 75% YOY. The strong performance was supported by higher defense demand, a recovery in commercial aerospace services, and continued momentum across its core segments.

Furthermore, RTX expects continued growth in 2026. The company guided for adjusted sales of $92 billion to $93 billion, and projected adjusted EPS of $6.60 to $6.80. RTX also anticipates free cash flow of $8.25 billion to $8.75 billion, reflecting strong demand visibility supported by its large order backlog and ongoing expansion in both defense and commercial aerospace markets.

Analysts predict EPS to be around $6.81 for fiscal 2026, up 8.3% YOY, before surging by another 10.1% annually to $7.50 in fiscal 2027.

What Do Analysts Expect for RTX Corporation Stock?

Recently, RTX Corporation received a price-target increase from Deutsche Bank to $240 from $235 while maintaining a “Buy” rating, citing the strong value proposition of the Hot Section Plus upgrade for the PW1100G engine.

On the other hand, last month, Jefferies reiterated a “Hold” rating and a $225 price target, reflecting a cautious outlook despite the stock’s strong gains over the past year.

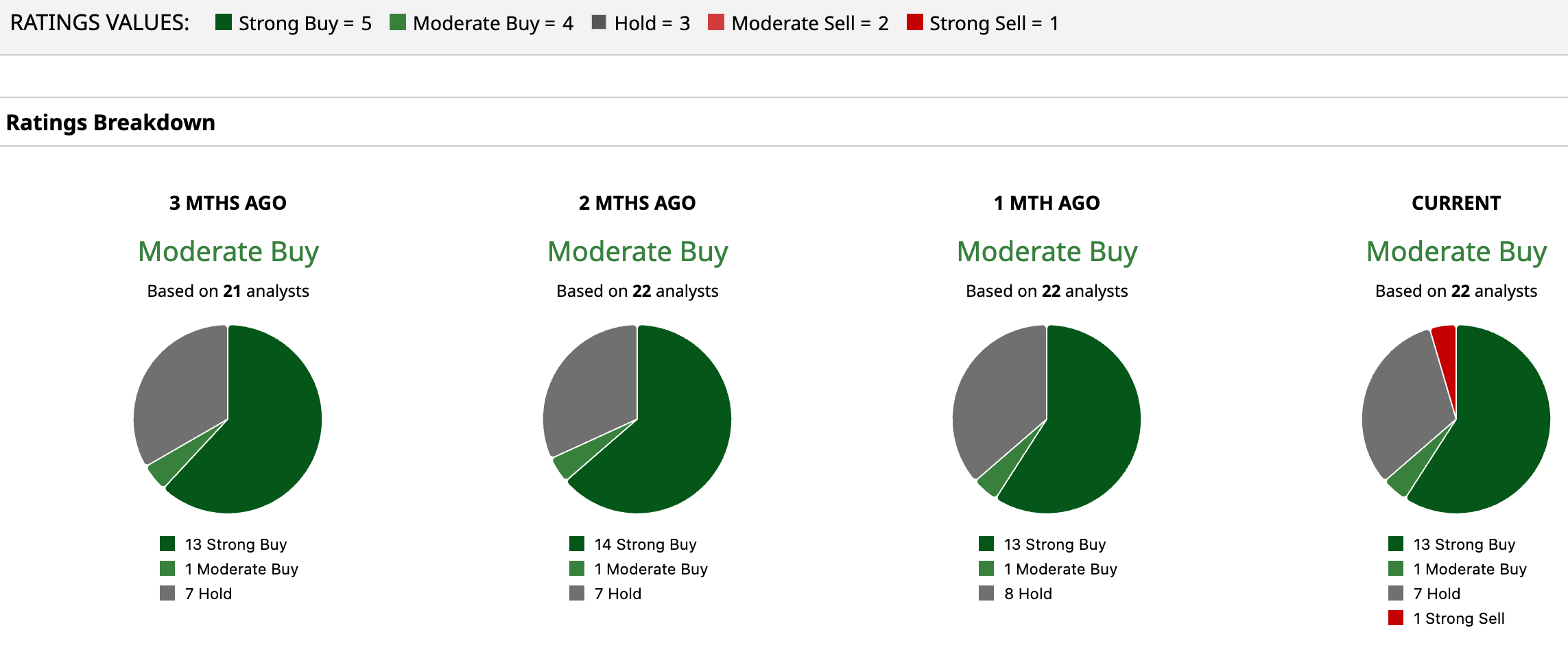

Overall, RTX has a consensus “Moderate Buy” rating. Of the 22 analysts covering the stock, 13 advise a “Strong Buy,” one suggests a “Moderate Buy,” seven analysts are on the sidelines, giving it a “Hold” rating, and one recommends “Strong Sell.”

The average analyst price target for RTX is $215.19, indicating a potential upside of 5.53%. Deutsche Bank’s Street-high target price of $238 suggests that the stock could rally 16.72%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- SoundHound Is One of the Most Short Stocks Right Now. Should You Bet on a SOUN Squeeze?

- Down 15% in 2026, Should You Buy the Dip in Microsoft Stock?

- 1 ‘Strong Buy’ AI Stock That Wedbush Loves Now: ‘No Lost Deals’ Amid ‘Disruption’

- Okta Is Pushing Higher. Should You Chase the Rally in OKTA Stock After Earnings Here?